50-Year Mortgages Are A Trap

With the Trump administration increasingly desperate to create any illusion of prosperity, a new proposal was introduced to create federally-backed 50-year mortgages to make housing “more affordable.” The plan promises lower monthly payments that Trump says would open the door to millions of would-be buyers priced out of the current market.

But as ultra-long term mortgages pump new money into the system, stretching loan terms will inflate home prices and transform the American dream of homeownership into a lifetime of debt servitude. It’s a Trojan Horse for monetary expansion.

With home prices near record highs and mortgage rates hovering near 6–7%, many households feel permanently locked out of the market. A 50-year term could reduce monthly payments by up to a third, depending on the loan size and interest rate. But the economic implications of lower monthly prices are massive inflation and higher prices in an already-cold economy.

For a $500,000 home financed at 6.3%, the total interest over a standard 30-year mortgage would amount to over $600,000. Extend that same loan to 50 years, and interest payments exceed $1 million, more than doubling the total cost of ownership. Add in property taxes for a home that both the government or the bank can take from you at any time, and it becomes difficult to view the scheme as a path to “ownership” at all.

The median age of home buyers is rising to about 40, which means that there will be 90-year olds living in assisted living facilities who are continuing to make payments. Alternatively, they will expire before their loan, passing the obligation onto their estate (read: their immediate families).

The borrower gains lower monthly payments, but pays the price through decades of compounding interest. The 30-year mortgage was a “policy innovation” of the 1930s, designed to stabilize a collapsing housing market. Before its introduction, most loans were often five years or less, and required large balloon payments at the end. The 30-year term tried to democratize homeownership by spreading costs predictably over time, nurturing the idea that the “American Dream” was inextricably linked with home ownership. It would be weaponized into a decades-long campaign to get as many Americans as possible locked into a debt cycle.

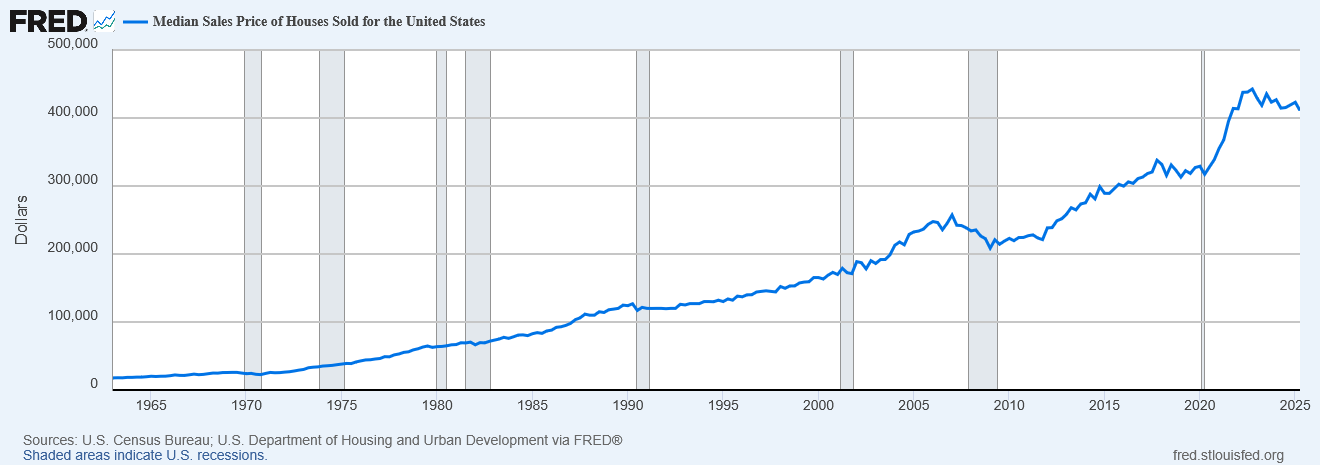

Median Sales Price of Houses Sold for the United States

It would also help entrench a system in which borrowing, rather than saving, became the dominant route to accessing American Prosperity. Extending that model by another 20 years is economic incrementalism, taking one of the roots of our current woes and doubling down on it..

The last time the U.S. experimented with mortgage innovation on a large scale was during the 2000s housing boom. Adjustable-rate mortgages, interest-only loans, and zero-down options expanded access to home ownership. Unfortunately, we all remember how that ended: a speculative bubble that culminated in the 2008 financial crisis. Although 50-year fixed-rate loans are structurally different, the underlying risk of overstimulating demand without addressing supply remains the same.

Restrictive zoning, high costs, and labor shortages are adding to all the other conditions that are already restricting home ownership. Adding longer mortgages makes the problem even worse. 50-year mortgages are money printing by a different name. By locking in customers for longer time periods, banks can make more loans and keep that newly-created money floating around the system for much longer.

Longer mortgages would also distort regional markets. In high-cost coastal areas such as California, New York, and Washington, where zoning and land scarcity already keep supply tight, 50-year mortgages could push prices even higher than in other areas. In more balanced markets like Texas or the Midwest, the effect might be smaller, but could still encourage speculative investment and be drastically inflationary. Developers might also build larger, more expensive homes to match inflated borrowing capacity, diverting resources from starter homes and affordable units.

Japan’s experiment with ultra-long mortgages offers a cautionary example. Faced with soaring property values, Japanese banks introduced 100-year mortgages, often structured to pass from parents to children. While these loans initially appeared to democratize ownership, they primarily benefited wealthier families using them for estate planning. Meanwhile, property prices remained inflated, and younger generations became increasingly priced out.

The United Kingdom offers another relevant case. In the early 2000s, several UK lenders began offering 40 and 50-year terms. As home prices continued to climb, affordability kept failing to keep up, and regulators later tightened lending standards. Many borrowers ended up refinancing repeatedly, effectively paying perpetual interest.

The U.S. national debt surpassed $36 trillion in 2025, and the Federal Reserve continues to grapple with inflation that they can’t control. Extending household debt horizons could intertwine private and public financial risks in subtle ways, as federally backed 50-year loans would expand the government’s exposure to interest rate fluctuations over an unusually long horizon. Even modest shifts in inflation could create serious long-term liabilities.

Ultra-long debt also discourages household saving. With income tied up in housing payments for five decades, families have less capacity to invest in retirement accounts, education, or small businesses. Are we solving affordability by expanding opportunity? Or feeding the same inflationary monster that got us here to begin with?

Less government intervention will improve housing affordability, not more. Government tinkering can’t bring balance to any market, and we’d be fools to think that housing is any different.