Why Hasn’t the Iran War Pushed Gold Even Higher?

Gold prices reached record highs in early 2026 following an epic 2025, fueled by central bank buying, inflation concerns, and demand for assets outside traditional finance. Since then, gold has pulled back significantly. Conditions created by the US-Iran war that began last February have contributed to this correction, but why?

While gold is usually pumped by geopolitical uncertainty, the conflict has led some governments and central banks to sell gold to meet short-term cash needs. Disruptions in the Strait of Hormuz have affected oil exports and energy supplies, putting pressure on budgets and foreign exchange reserves.

Governments have prioritized rebuilding fuel supplies and stabilizing currencies, which requires dollars more than long-term stores of value in the short term. And with higher oil prices threatening to rip higher still, markets are considering the prospect of central bank interest rate hikes to counteract rising inflation.

Turkey has sold or lent gold reserves to support the lira amid economic pressures from higher energy costs. Russia has also reduced holdings to address fiscal demands. These sales have added to supply in the market at a time when gold entered the conflict period looking technically overbought after its prior rally.

When dollar shortages emerge due to disrupted oil revenues, governments turn to gold as a funding source, especially after a historic bull run that allows them to take equally-historic profits. Persian Gulf states and others facing liquidity needs have used gold holdings to generate cash rather than holding it purely as a safe haven. It’s a reminder of gold’s role both as a safe haven and as a reserve asset that can be mobilized during times of stress.

In past times of fiscal strain, governments have turned to gold reserves or private holdings to raise funds. During the Great Depression, the U.S. government under President Roosevelt required the surrender of gold holdings through Executive Order 6102 in 1933, followed by the Gold Reserve Act of 1934. These strong-arm tactics allowed the government to revalue gold and use the proceeds to support spending and debt management. While the context differs, the principle is the same: when immediate cash requirements arise, gold can be sold or mobilized.

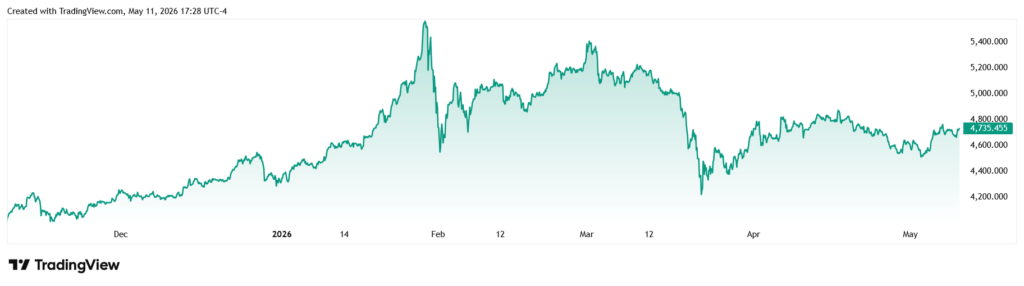

Gold vs USD 6-Month

Central bank behavior in 2026 reflects a mix of trends. Many central banks in emerging markets continue to add gold to diversify away from the U.S. dollar and manage risks from higher inflation and geopolitical tensions. Net purchases have remained positive overall in recent quarters, with countries like China and Poland among the buyers. However, sellers driven by wartime or currency pressures have created temporary downward influence on prices.

Gold and silver have seen volatile trading in 2026 after such a strong 2025. The metals entered the conflict overbought on the technical side, leading to profit-taking and consolidation. Higher oil prices from the war have temporarily supported a stronger dollar and raised expectations for interest rates in some economies, which has weighed on gold.

But gold has continued to serve as a hedge in other ways. Investors and central banks have used it to rebalance portfolios during equity selloffs and to diversify reserves away from dollar-denominated assets. Long-term drivers, like structural inflation concerns, central bank diversification, and demand for physical assets, remain firmly in place. Meanwhile, bond yields will keep going up. As Peter Schiff recently said on X:

Soaring deficits, a falling dollar, rising inflation, and eroding confidence in the fiscal position of the U.S. will continue putting upward pressure on long-term yields.

As governments address fuel supply rebuilding and short-term liquidity in the wake of Iran war disruptions, selling pressure on gold has been a natural outcome. This does not diminish gold’s role as a safe-haven asset over time. Once the conflict eases and the fog of war lifts, the conditions that supported the prior rally can reassert themselves. Expect the bull run in gold to resume as peace prospects reduce immediate liquidity demands and allow investors to refocus on underlying fundamentals.

The recent price action highlights gold’s dual nature and is positive, not negative. The yellow metal functions as both a long-term store of value and a liquid asset that governments and institutions can access when cash is badly needed. The correction after the epic rally, combined with targeted selling by some central banks, has fueled this period of consolidation. As the Iran war comes closer to a resolution, the structural demand for gold, from central banks seeking alternatives to the dying dollar and investors protecting against inflation, will spark renewed upward movement.

The recent decline in gold prices reflects practical responses by governments and central banks to cash needs during wartime disruptions, not a fundamental rejection. Past rallies have included similar pauses, and the drivers for higher prices persist. When the immediate pressures from the conflict subside, gold’s role as a key reserve asset is going to help drive the next phase of its bull market, especially as the money supply expands further and inflation continues to rip.