As Inflation Keeps Rising, Americans Have No Savings

American households are plummeting to razor-thin financial margins as the personal savings rate falls to numbers last seen before COVID.

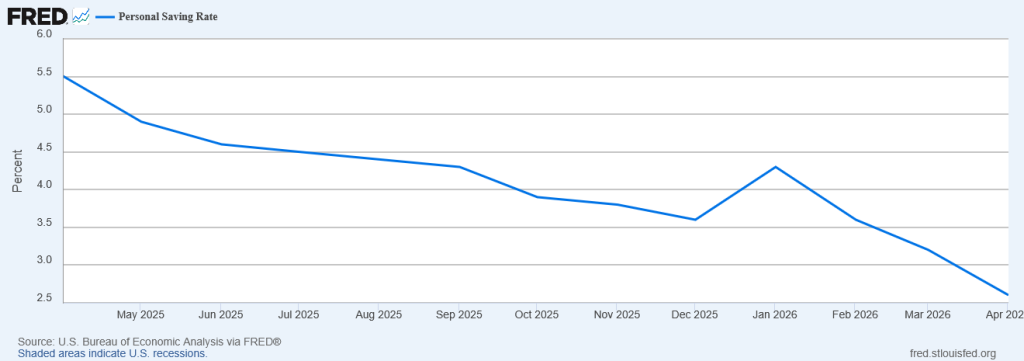

Personal savings fell from around 4.3% of disposable income in January to just over 2.5% in April, all as the cost of living continues to climb. Americans are drawing down reserves to cover groceries, housing, transportation, and insurance, with nothing left over for unexpected expenses (much less investing).

With savings accounts in a sharp decline, there isn’t much room to go lower.

US Personal Saving Rate, 1-Year

Source: U.S. Bureau of Economic Analysis, Personal Saving Rate [PSAVERT], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/PSAVERT, June 8, 2026.

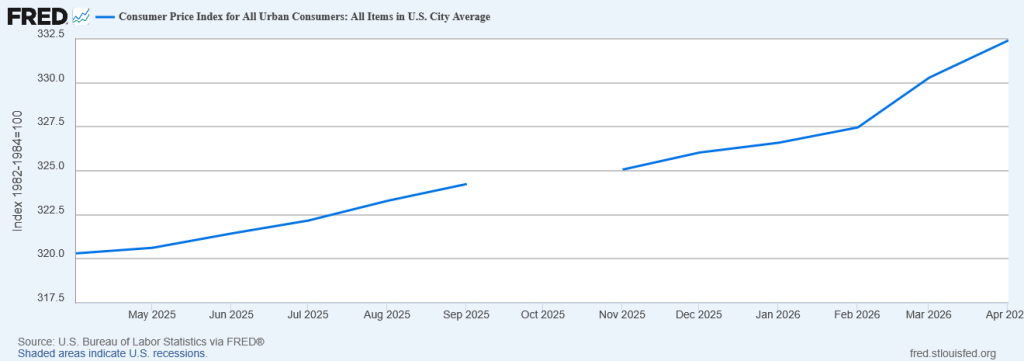

Wage growth hovers around 3.4%, yet recent inflation readings sit at around 3.8% (if you believe the understated official inflation data). Those inflation numbers will only get higher, squeezing real purchasing power to an unsustainable brink.

Consumer Price Index for All Urban Consumers: All Items in US City Average

Source: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average [CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CPIAUCSL, June 8, 2026.

Meanwhile, people are taking out more loans on their 401(k) accounts and becoming delinquent on credit card and auto debt. With consumer spending propping up US GDP, rising prices across the board have forced a change to the traditional emergency fund guidelines, which say to maintain three to six month’s living expenses.

The goalposts have been reset. Even for the bare minimum of three to six months of expenses forming still the baseline for a viable emergency fund, the new view is that Americans require $20,000 or more in liquid savings to fulfill that requirement.

Asset owners may see gains in equities and real estate, but wage earners and those relying on fixed incomes experience steady erosion of their financial position. Peter Schiff has warned for some time that stagflation is here, and the writing is on the wall that it will eventually intensify into a full-blown crisis.

If you think gold, silver, oil, and Treasury yields are high now, they all look like they’re about to explode much higher. The same is true for consumer prices in general, as inflation returns with a vengeance. This does not portend 1970s stagflation. It portends something worse.

Recent data aligns with that view. Consumer sentiment has hit record lows while inflation reaccelerates. Downward revisions in GDP and jobs data are almost guaranteed to follow once the market digests the initial, rosier numbers.

Structural issues abound: massive government deficits, monetary accommodation, major wars, and supply pressures. In our stagflation, like many others throughout history, official figures mask the extent of the weakness in Main Street while wages sputter and prices for essentials keep climbing.

With inflation and recession conspiring to force a policy response, the Federal Reserve and other interventionary institutions can only prevent a recession today by guaranteeing an even bigger one later.

Other countries aren’t buying and holding US debt like they used to. A crisis is unavoidable the moment big buyers of US debt decide that it’s no longer worth the risk to put “full faith and credit” in America’s ability to make good on her promises.

Higher energy costs feed into price increases for practically everything else. Rents, food, utilities, construction costs, and insurance premiums are all going up. Even as some sectors post strong corporate profits, especially those tied to manic AI enthusiasm, the broader picture shows households struggling for the basics.

Confidence is fading as savings dwindle and savers are constantly being punished. Cash and low-yield deposits will lose ground while debt servicing costs remain elevated, with high credit card rates contributing to a cycle where people spend what they have just to maintain their current standard of living.

Expansionary monetary policy lowers the purchasing power of every dollar, but official CPI readings don’t show what real Americans are experiencing at the household level when it comes to feeding their kids, heating their homes, and saving for a future that actually feels hopeful.

Unlike central banks, you can’t print money, but you can protect yourself with gold when the Fed’s printing keeps pushing us toward the inevitable conclusion of their own experiments.

Receive SchiffGold’s key news stories in your inbox every week – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold and buy silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!