Propping Up the Yen, Again and Again

Can Japan just keep propping up the yen forever?

At a certain point, Japan won’t be able to just keep dumping dollars and Treasuries to prevent its currency from imploding.

With an economy so sensitive to rate hikes after decades of zero-interest rate policy, the Bank of Japan can’t endlessly jack up the cost of borrowing without risking severe consequences. And, even if Washington could be convinced to do so, the US Treasury and Fed can’t save Japan by buying yen directly without spiking yields and weakening the relative strength of the dollar.

Japan’s repeated attempts to defend the yen through interventions are going to hit a wall of reality built from decades of ultra-loose policy, massive debt, and a collision with unyielding global forces. As Japanese Finance Minister Satsuki Katayama has affirmed, Japan stands ready to act against excessive forex volatility, emphasizing interventions that avoid spiking Treasury yields. But she walks an impossible tightrope. Foreign governments led by Japan and China are offloading Treasuries to defend their currency from oil shocks amid the ongoing conflicts in the Middle East.

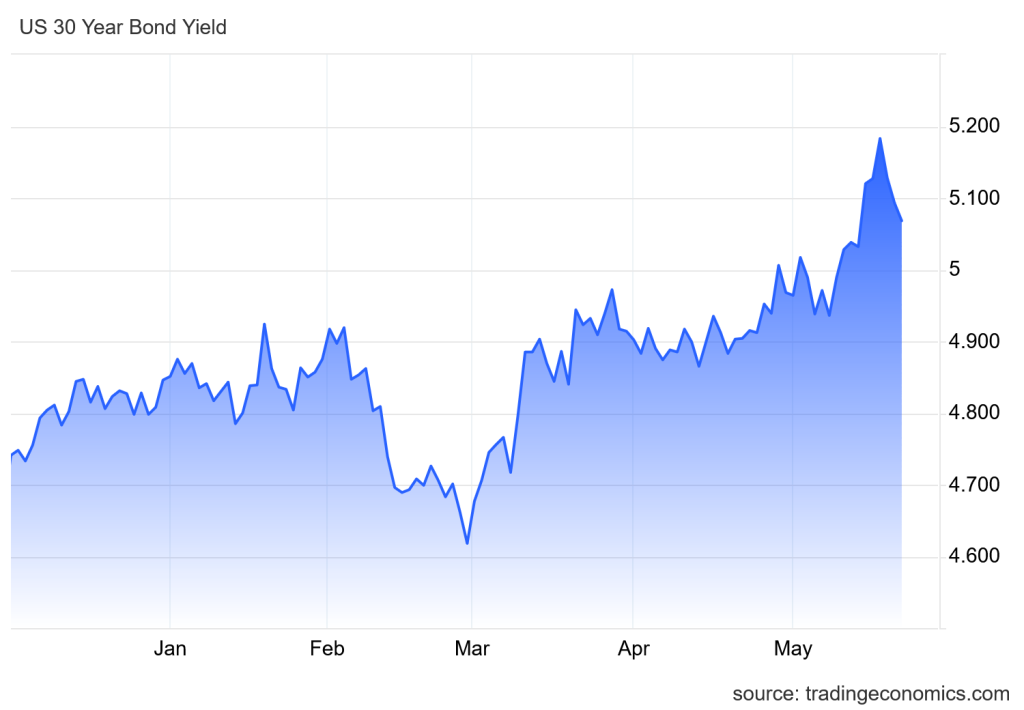

As the largest foreign holder of US debt, every yen-support operation out of Japan is a potential accelerant for higher yields. In March alone, Japan shed about $47 billion in Treasuries, dropping to $1.191 trillion, as it battled yen weakness past sensitive levels amid surging energy import costs. They’re liquidating dollar assets to buy yen, directly feeding into a Treasury market already flashing warning signs. Now Treasuries have entered a “danger zone” of surging long-term yields, with the 30-year yield recently pushing above 5.2%, its highest since 2007, while the 10-year climbed toward 4.7%.

HSBC and others warn that further repricing of terminal rates could hammer risk assets. The bond vigilantes are waking up to sticky inflation, geopolitical oil spikes, and endless deficits, and Japan dumping more paper to prop up its currency (yet again) adds more powder to the keg. At what point does the feedback loop break?

Peter Schiff has been ringing the alarm bells about Japan unloading US debt. The risks of Tokyo selling US Treasuries to fund stimulus or interventions are clear, at a time when the US can’t afford it:

That will send US bond yields higher and the dollar lower, worsening stagflation.

Japan needs a weaker yen for exports but can’t tolerate a collapse, so it intervenes, selling Treasuries that push yields up and complicate the same dollar dynamics it relies on. It’s a contradiction where the math can only lead to one possible outcome: a race to the bottom. You can perform a high-wire act with no net and get away with it for one show, maybe two shows, or maybe even a hundred. But eventually, the audience is going to witness something horrible. Every time the yen needs to be rescued again, we come a little bit closer to the inevitable end result.

Japan isn’t alone, either. De-dollarization is picking up steam across the world, and China joined its historical rival by slashing its Treasury holdings to $652 billion and change in March, the lowest since 2008, as part of a broader foreign retreat from US debt. Oil price surges from tensions in the Gulf forced energy-dependent importers to tap reserves for currency defense. With dropping foreign holdings, valuation losses compound the pain as bond prices fall.

30-Year Treasury Yields, 6 Month

De-dollarization is a pragmatic choice when foreign nations see US debt exploding toward $40 trillion, with crushing interest expenses. When your biggest holders start selling to defend their own currencies, the “exorbitant privilege” of the dollar begins to look more like an exorbitant burden.

Meanwhile, real rates are collapsing even as nominal yields rise, because inflation is outrunning them. PPI data has shown explosive month-over-month jumps, with producer prices rising year-over-year and core figures annualizing far hotter. Import and export prices are both climbing. Algorithms might sell gold on higher nominal yields, but negative or plunging real rates are screaming for hard assets.

Japan’s problem runs deeper than one-off interventions. Years of negative rates, massive QE, and demographic headwinds have left it with an enormous amount of government debt relative to GDP. The Bank of Japan owns a huge chunk of its own bonds, distorting markets. When external shocks like oil spikes hit, the yen buckles, forcing choices between more domestic monetization (which weakens the currency further) or selling foreign reserves. Recent verbal and actual interventions have bought time, but time is expensive.

Sustained Treasury sales risk higher US yields, which could ripple back through global carry trades and funding costs. Japan’s own bond yields creeping higher add internal pressure, since breaches in JGB yields could unwind the yen carry trade that has propped global assets for years. A reversal there would be a margin call heard worldwide.

Investors are demanding better compensation amid uncertainty. No one wants to hold paper when inflation is eating returns and geopolitics is adding volatility. For Japan, the dilemma is acute: they can defend the yen today at the cost of higher global rates and potential retaliation, or let it slide and risk imported inflation plus corporate pain.

America isn’t insulated. With debt approaching unsustainable territory and interest costs already exceeding a trillion annually in some measures, higher yields from foreign selling are a nightmare scenario. The Fed faces an impossible trinity: ease to cap yields and risk more inflation and dollar weakness, or hold firm and watch funding costs explode. As Peter Schiff warned earlier this month, the dollar is on the brink of a broader sovereign debt and currency crisis:

We are not in a position to pay that kind of debt. In fact, the only reason we’ve been able to sustain $20, $30, now $40 trillion-dollar national debt is that interest rates have been so low…well, those low interest rates are rapidly becoming a thing of the past. The rug is getting pulled out from under the United States.

Bond yields are too low for the very real and present risks of default or inflation erosion. Holding US debt is becoming a burden. With real rates collapsing while markets focus on nominal figures, gold is seeing what might be its biggest setup yet:

All of our avenues for borrowing money are being cut off. The Chinese aren’t lending us the money anymore. The Japanese, not only can not lend us money, they’re going to start selling US Treasuries because they’ve got a problem of their own, and the best way out is to sell our bonds.

Central banks have been net gold buyers, but the shift to private and institutional demand could accelerate if confidence in fiat erodes further. Gold doesn’t care about G7 communiques or intervention rhetoric; it responds to purchasing power loss, and for the Fed, the only way out is aggressive expansion of stealth QE.

Beyond Japan and the US, this is all a symptom of a fiat system stretched thin by endless stimulus, geopolitical fractures, and eroding trust. China reducing exposure, other nations recalibrating, and oil acting as a catalyst are all signs of fundamental fragmentation. The old way of endlessly recycling dollars into Treasuries is breaking, and diversification into productive assets and real money just makes sense when paper promises face those kinds of stress tests.

The yen interventions might stabilize short-term FX charts, but they can’t fix underlying imbalances caused by Japan’s debt load, America’s sky-high deficits, global energy dependencies, and monetary policy that prioritizes kicking the can.

Japan can’t dump Treasuries indefinitely without consequences. The US can’t run trillion-plus deficits forever. Central banks can’t print without inflation consequences that real rates reveal. No system built on endless intervention lasts forever, and with cracks visible in yield curves, reserve shifts, and inflation, smart capital is positioning away from crowded paper trades and toward true scarcity and intrinsic value.

The coming repricing won’t be gentle.

Receive SchiffGold’s key news stories in your inbox every week – click here – for a free subscription to his exclusive weekly email updates.

Interested in learning how to buy gold and buy silver?

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!