Fed Talks Tough But Money Supply Explodes Higher

Money Supply is a very important indicator. It helps show how tight or loose current monetary conditions are regardless of what the Fed is doing with interest rates. Even if the Fed is tight, if Money Supply is increasing, it has an inflationary effect.

One key metric shown below is the “Wenzel” 13-week annualized money supply figure. It was made popular by the late Robert Wenzel who tracked the metric weekly as an indicator for where the economy might be headed. In 2020, the Fed started reporting the data monthly instead of weekly. It should also be noted that Money Supply data can be heavily revised in future months.

Recent Trends

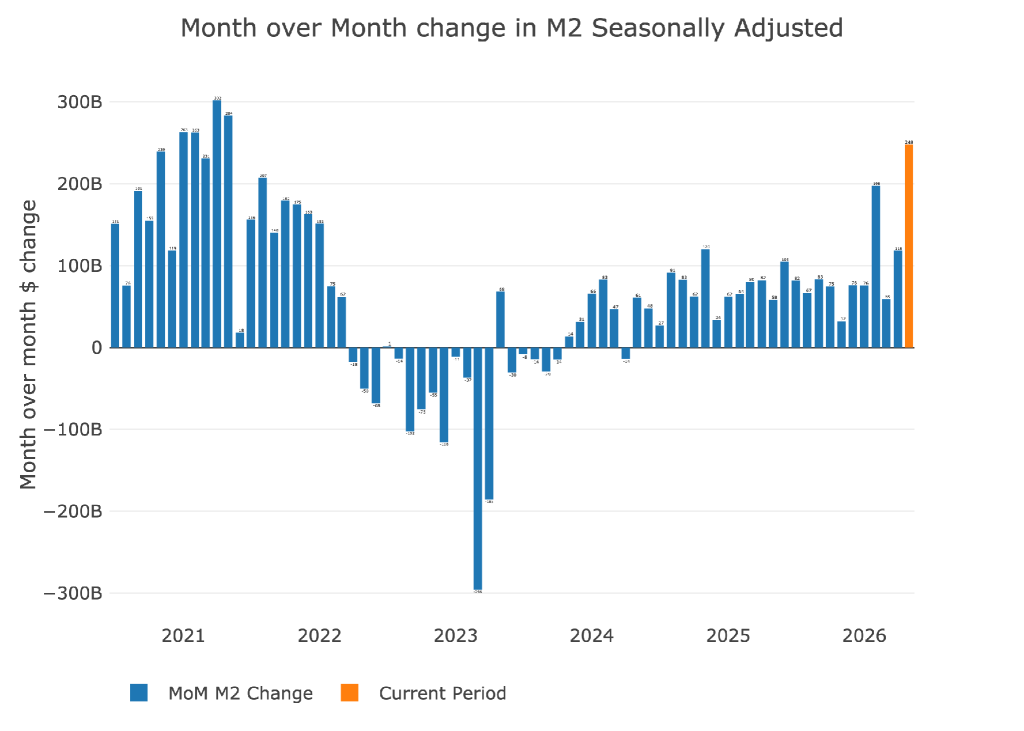

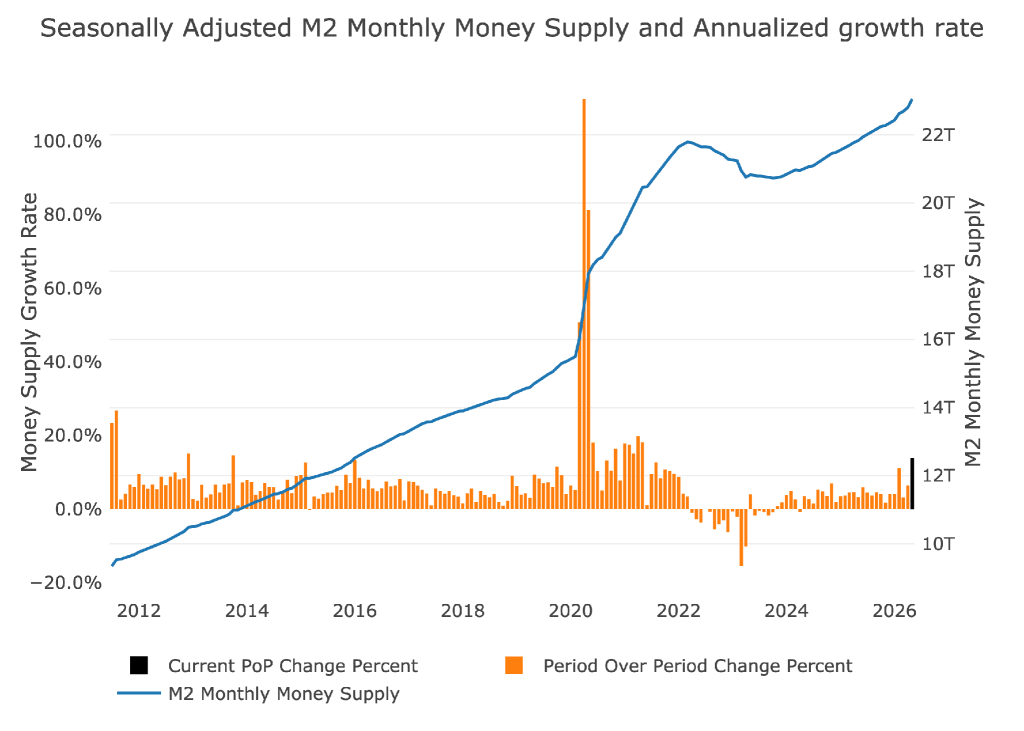

Seasonally Adjusted Money Supply has been growing on a consistent monthly basis since November 2023. The latest month (May) showed growth of $248B which is the strongest single month going back as far 2021 when the Fed was making it rain money.

Warsh spent his entire speech last week explaining how the Fed was going to get tough on inflation and yet May was head and shoulders above nearly every month since 2021. Arguably, he came in at the end of the month and has not had time to leave his fingerprints on policy, but the irony should not be lost on anyone.

Figure: 1 MoM M2 Change (Seasonally Adjusted)

The increase in May was 13.8% annualized, which is miles higher than any of the trailing period trends.

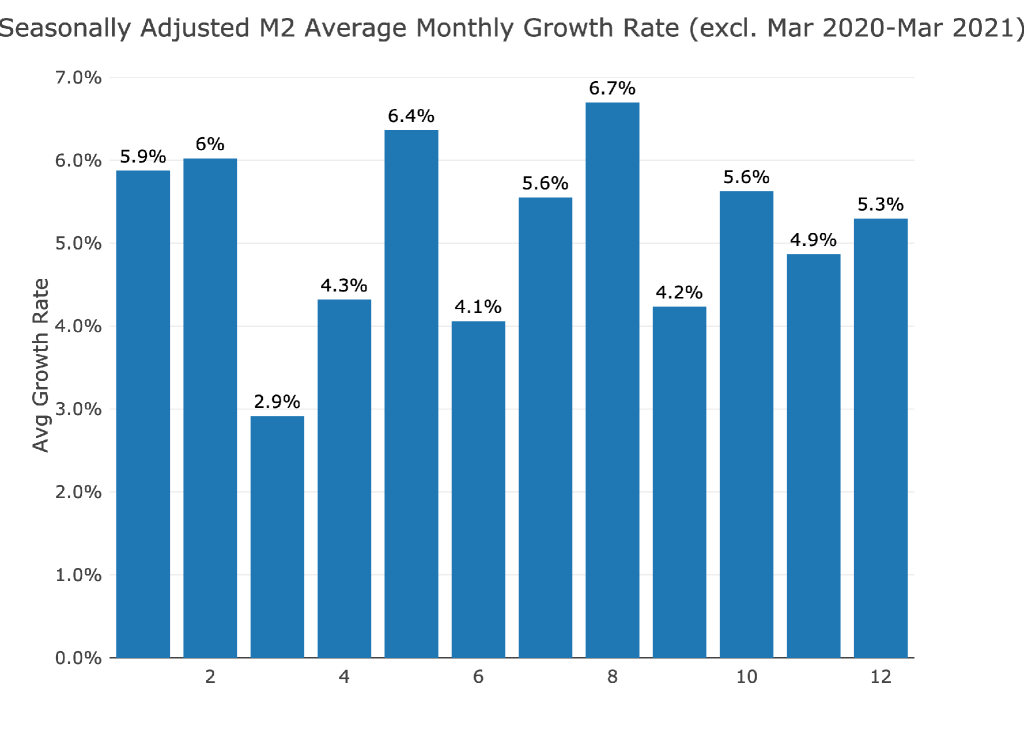

Figure: 2 M2 Growth Rates

May is one of the stronger months of the year typically, but this May was more than double the average.

Figure: 3 Average Monthly Growth Rates

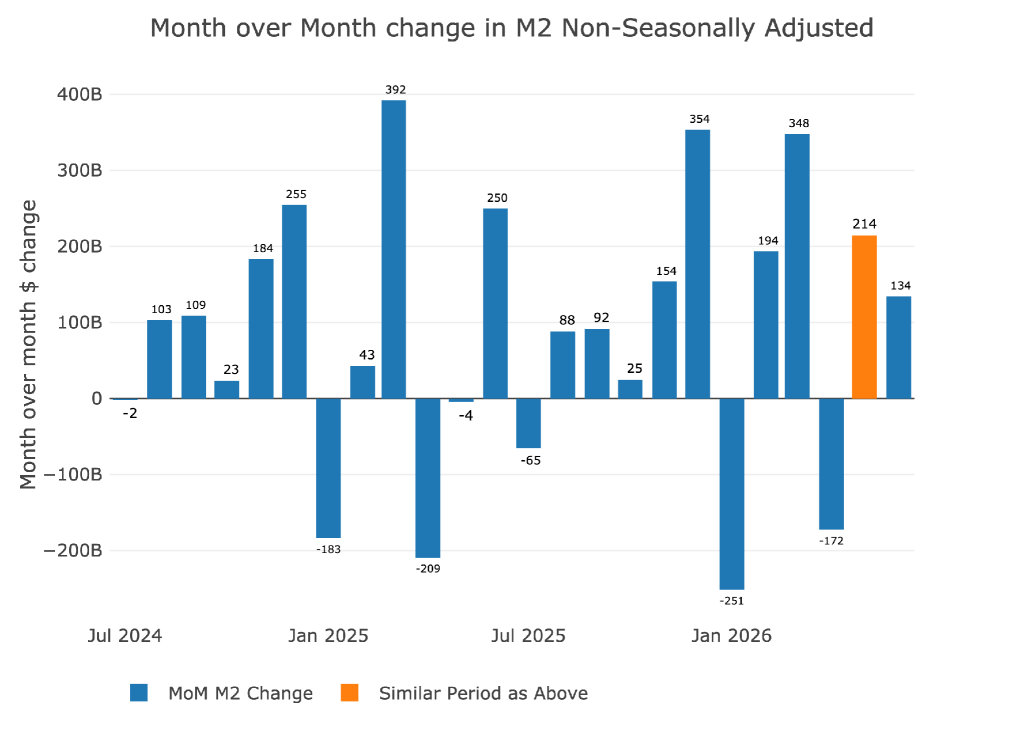

Non-seasonally adjusted shows that May (orange bar) is not nearly as strong when compared to other recent months (note: this data is ahead of the seasonally adjusted data above).

Figure: 4 MoM M2 Change (Non-Seasonally Adjusted)

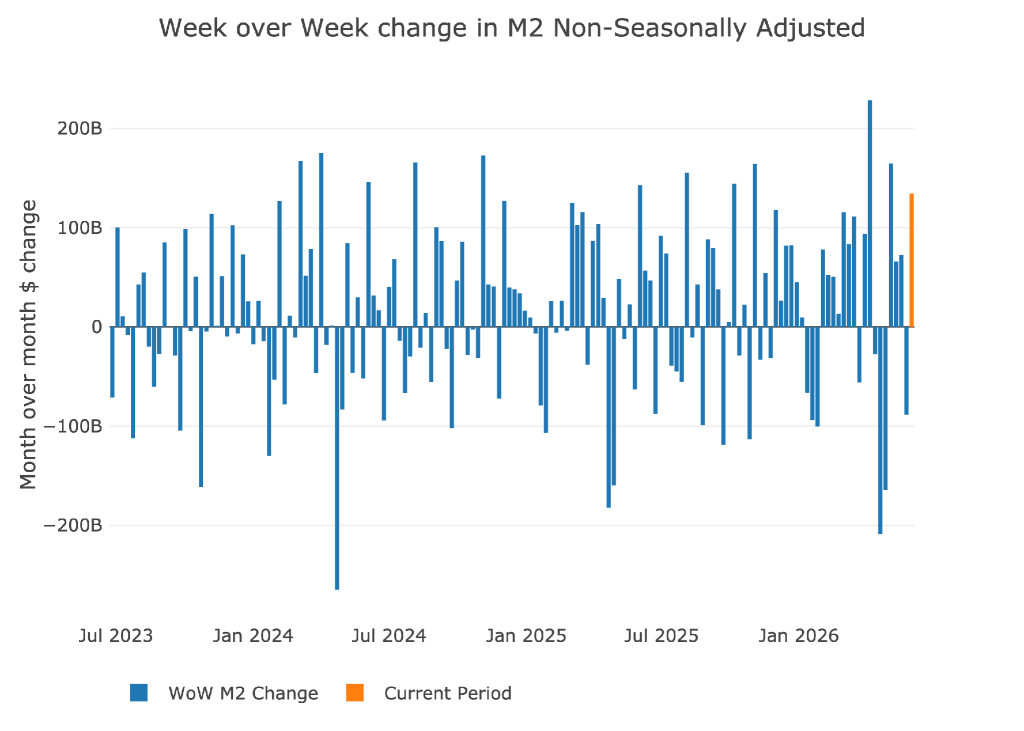

The weekly data shows what happened: May only saw one down week with the other three weeks exhibiting strength.

Figure: 5 WoW M2 Change

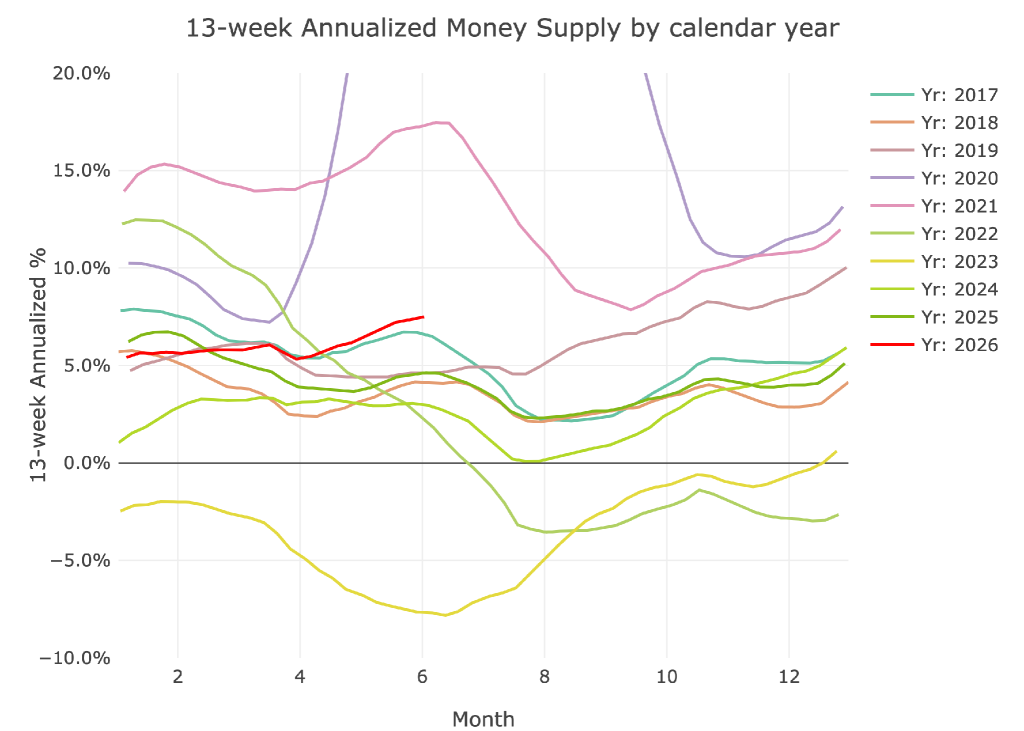

The “Wenzel” 13-week Money Supply

The late Robert Wenzel of Economic Policy Journal used a modified calculation to track Money Supply. He used a trailing 13-week average growth rate annualized as defined in his book The Fed Flunks. He specifically used the weekly data that was not seasonally adjusted. His analogy was that in order to know what to wear outside, he wants to know the current weather, not temperatures that have been averaged throughout the year.

The objective of the 13-week average is to smooth some of the choppy data without bringing in too much history that could blind someone from seeing what’s in front of them. The 13-week average growth rate can be seen in the table below.

Growth had been relatively flat for about 20 weeks ranging around 5-6%. Growth has accelerated out of this range to 7.5% in the latest reading. This is the fastest growth since 2022.

Figure: 6 WoW Trailing 13-week Average Money Supply Growth

The plot below shows how the latest year compares with previous years. You can see how 2026 has edged out of a range that it has been trapped in for some time. Based on seasonal trends, there should be a dip in the coming months, so this will be more telling of the direction of the Fed.

Figure: 7 Yearly 13-week Overlay

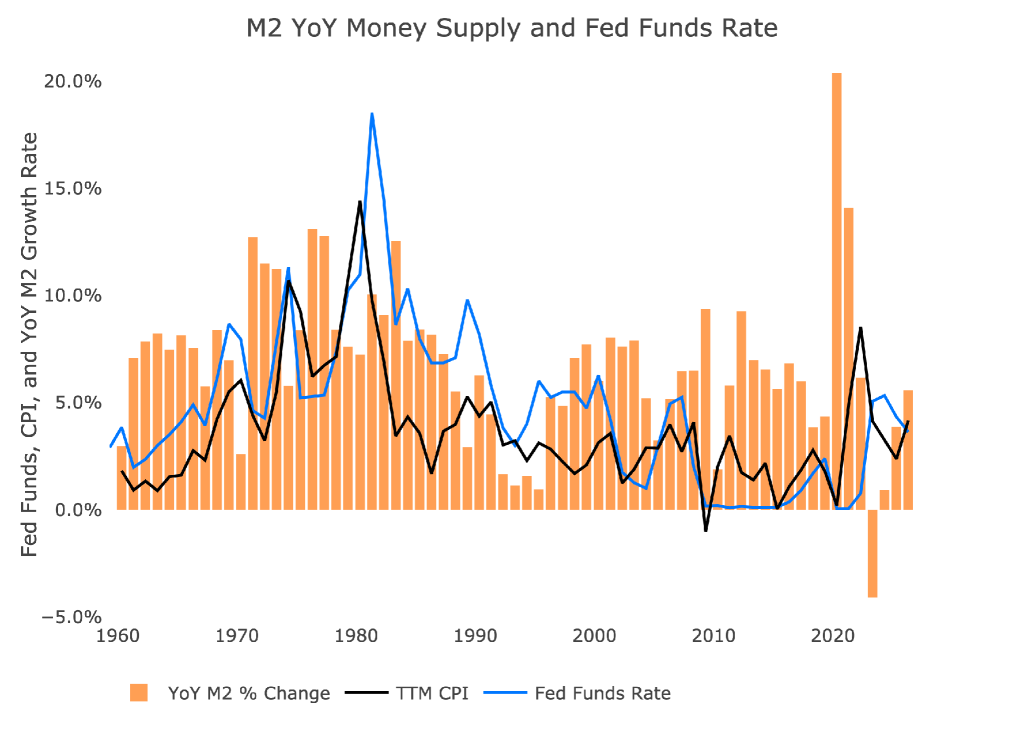

Inflation and Money Supply

The chart below shows the history of inflation, Money Supply, and Fed Funds. As shown, in 1970 inflation worked with a ~2 year lag compared to Money Supply. Money Supply slowed dramatically in 2023 and 2024 but has been moving back up. Inflation has also been stickier than the Fed would like, but unfortunately, they cannot do much given the large debt load of the US Government and Corporations. Despite inflation staying elevated, even moving up in the recent period, the Fed has no choice but to continue lowering rates.

The inflation rate is now above the Fed Funds. The inflation rate is now 4.2% which is 60 bps above the Fed Funds rate of 3.6%. The inflation rate has remained above 2% for 5 years now, proving much stickier than anyone originally forecast. This flip is likely why the market is now pricing in the distinct possibility of a rate hike before the end of the year.

To get inflation back down, rates need to be significantly higher than the rate of inflation, so the Fed would need to raise rates by at least a full percentage point, and likely more.

Figure: 10 YoY M2 Change with CPI and Fed Funds

Historical Perspective

The charts below are designed to put the current trends into historical perspective. The orange bars represent annualized percentage change rather than raw dollar amount. You can see that the Money Supply has stayed at a positive and consistent growth level. This is not a good sign if inflation needs to be coming down.

Figure: 9 M2 with Growth Rate

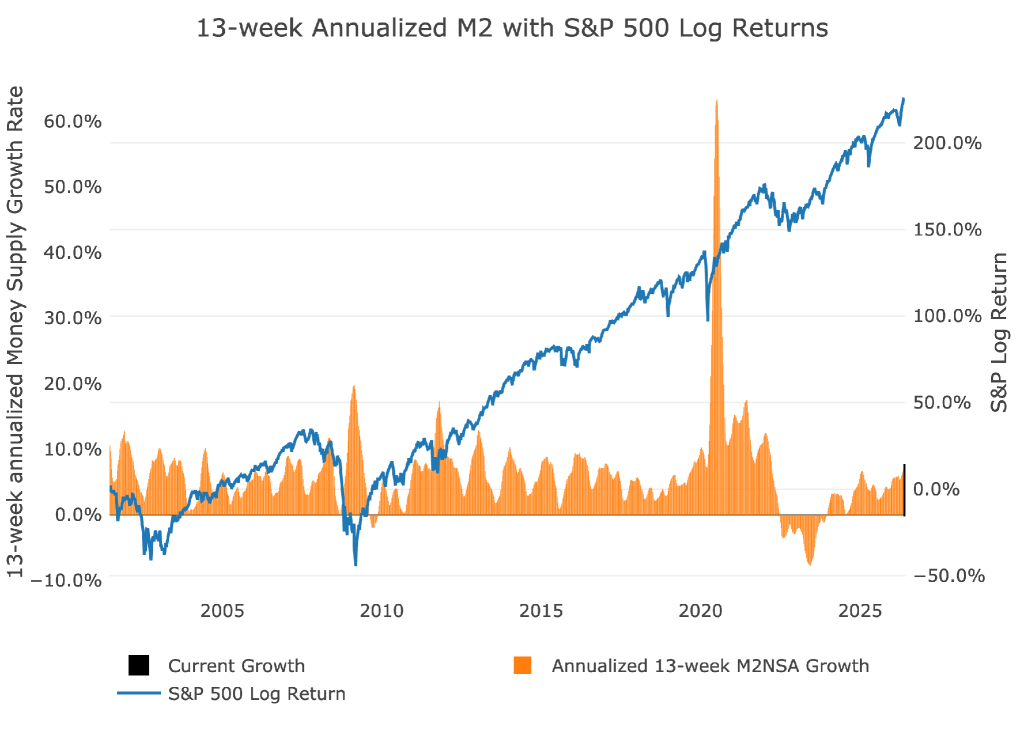

Below shows the 13-week annualized average over history. This chart overlays the log return of the S&P. Mr. Wenzel proposed that large drops in Money Supply could be a sign of stock market pullbacks. His theory, derived from Murray Rothbard, states that when the market experiences a shrinking growth rate of Money Supply (or even negative) it can create liquidity issues in the stock market, leading to a sell off.

While not a perfect predictive tool, many of the dips in Money Supply precede market dips. Specifically, the major dips in 2002 and 2008 from +10% down to 0%. 2022 was highly correlated with a fall in Money Supply and the rebound has corresponded with the big stock market move we saw in 2023 and into 2024.

More liquidity getting pumped into the economy helps explain why the market continues to reach all-time highs despite all the headline risk. With the war still on, oil prices reaching multi-year highs, and a ton of uncertainty, one would expect the market to be under pressure. But the added money supply growth is helping support the market.

Please note the chart only shows market data through June 1st to align with available M2 data.

Figure: 10 13-week M2 Annualized and S&P 500

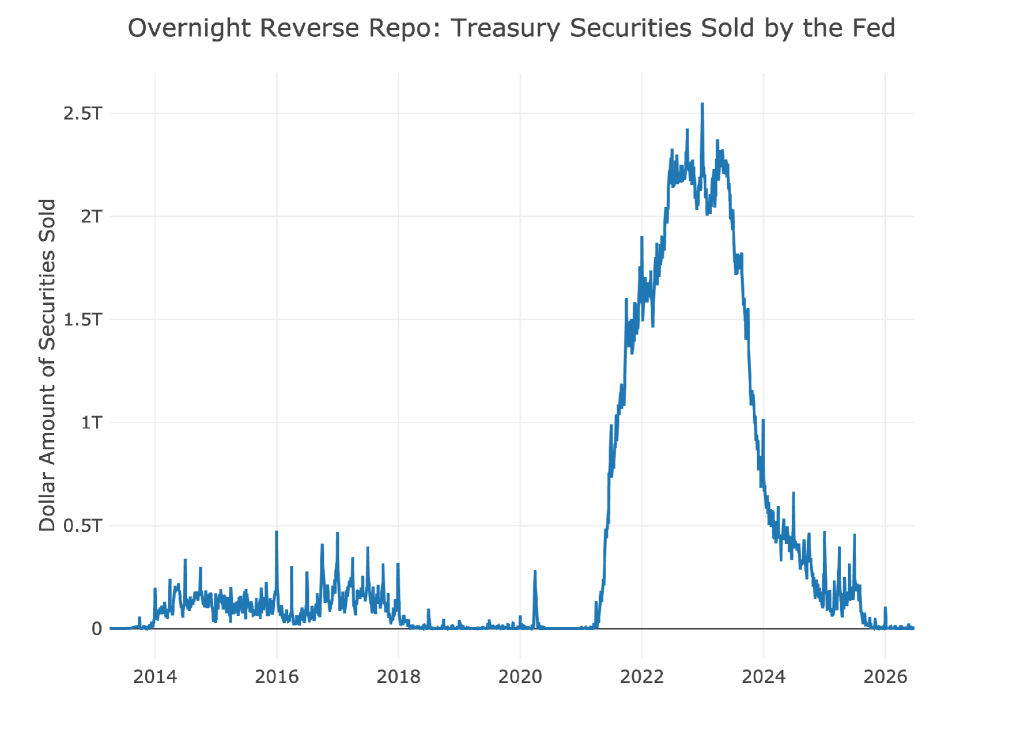

One other consideration is the reverse repo market at the Fed. This is a tool that allows financial institutions to swap cash for instruments on the Fed balance sheet.

Reverse Repos peaked at $2.55T on Dec 30, 2022. Money gushed out from March 2023 to May 2024. The balance now sits close to zero.

Figure: 11 Fed Reverse Repurchase Agreements

Wrapping Up

It will take time for Kevin Warsh to leave his fingerprints on the Fed. But it is much easier to talk tough than act tough. To act tough on inflation, the Fed needs to be shrinking the money supply. At this stage of the inflation cycle, simply letting growth slow will not be enough. However, shrinking the money supply is going to be extremely difficult. Raising rates and turning off the new QE will be the start. Warsh will realize pretty quickly that the outcome is going to be too painful for the economy to handle.

Bottom line, gold and silver are under pressure on tough talk. The market has not seen through to the other side yet and when it does, the metals are going to explode higher.