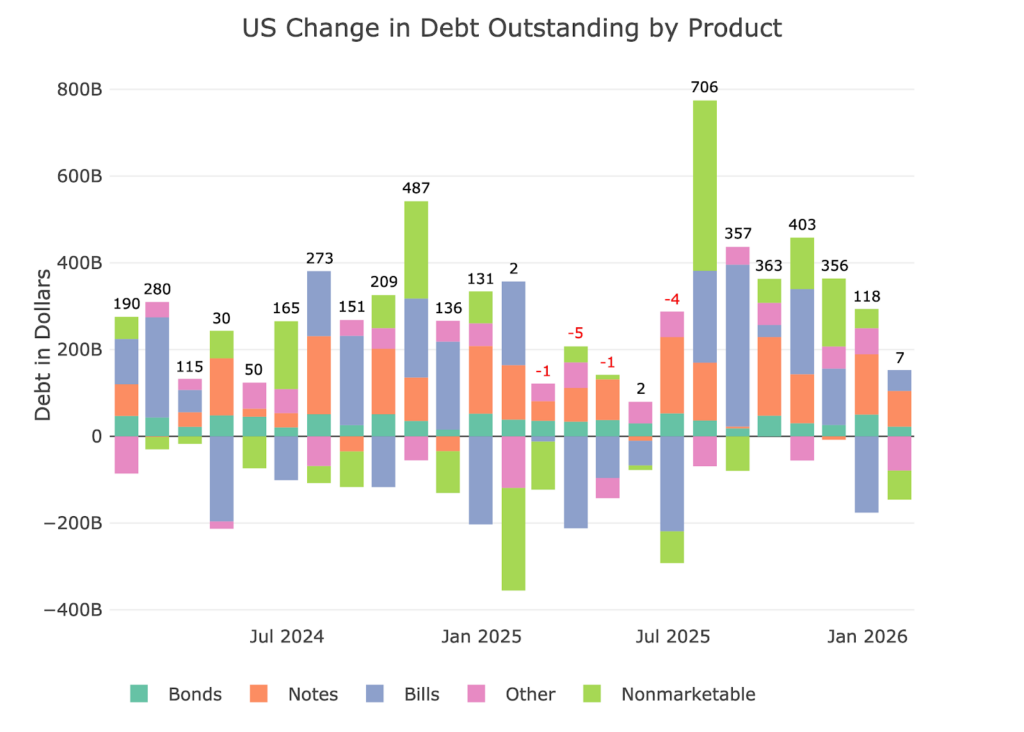

US Government Adds $481B in Debt in 3 months

Current Trends

The government hit the debt ceiling back in January which blocked any net new debt from being created from January to June. Once the debt ceiling was lifted, the government wasted no time in catching up for all the months where borrowing was frozen. Over the last 7 months, the government borrowed an incredible $2.28T!!

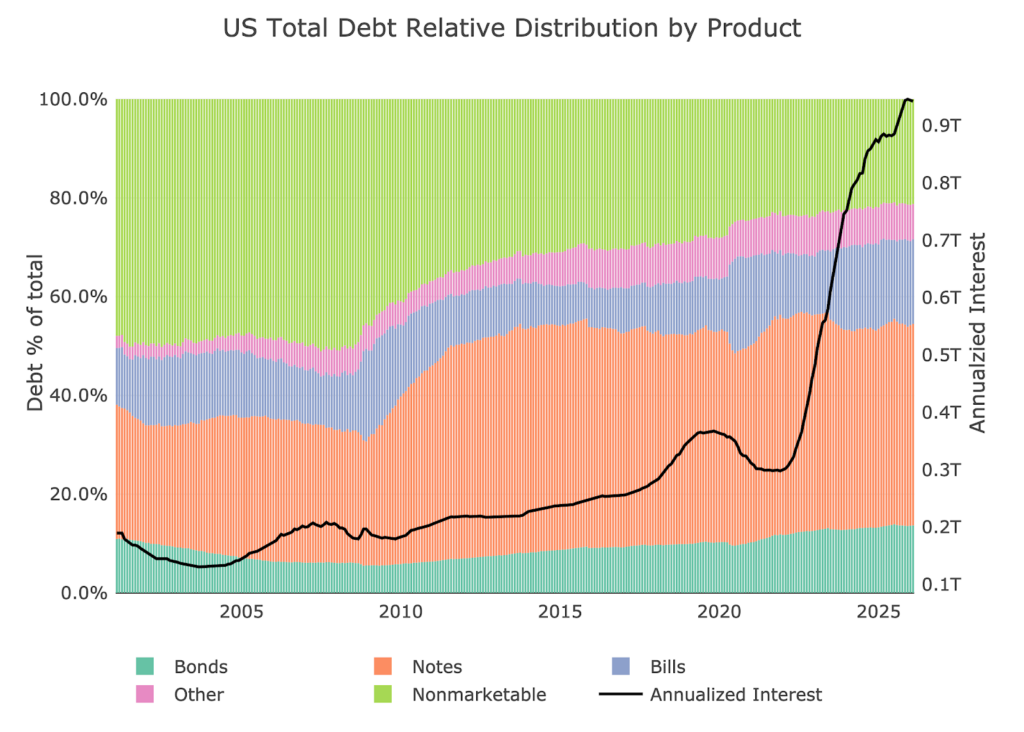

Note: Non-Marketable consists almost entirely of debt the government owes to itself (e.g., debt owed to Social Security or public retirement)

Figure: 1 Month Over Month change in Debt

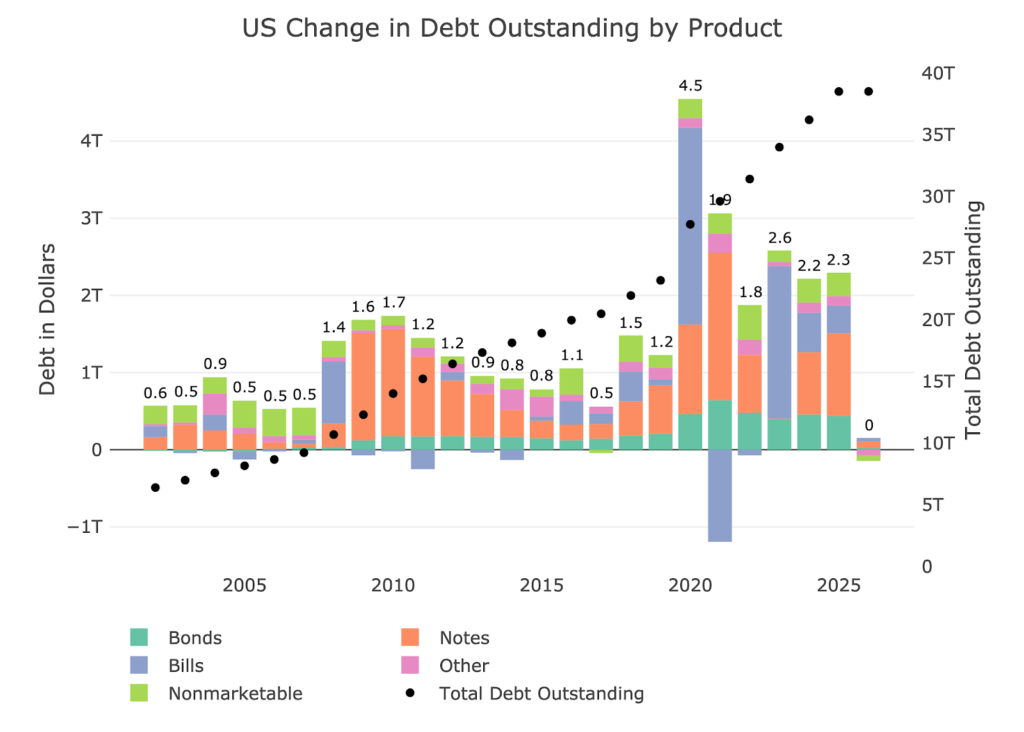

January was a very small month, but the chart below shows that $2.3T was borrowed for all of 2025. This follows $2.6T and $2.2T in 2023 and 2024. Needless to say, there seems to be a new standard of $2T+ annual borrowing. This will likely mean adding $10T every 4 years at current rates. More than likely that is going to accelerate going forward.

Figure: 2 Year Over Year change in Debt

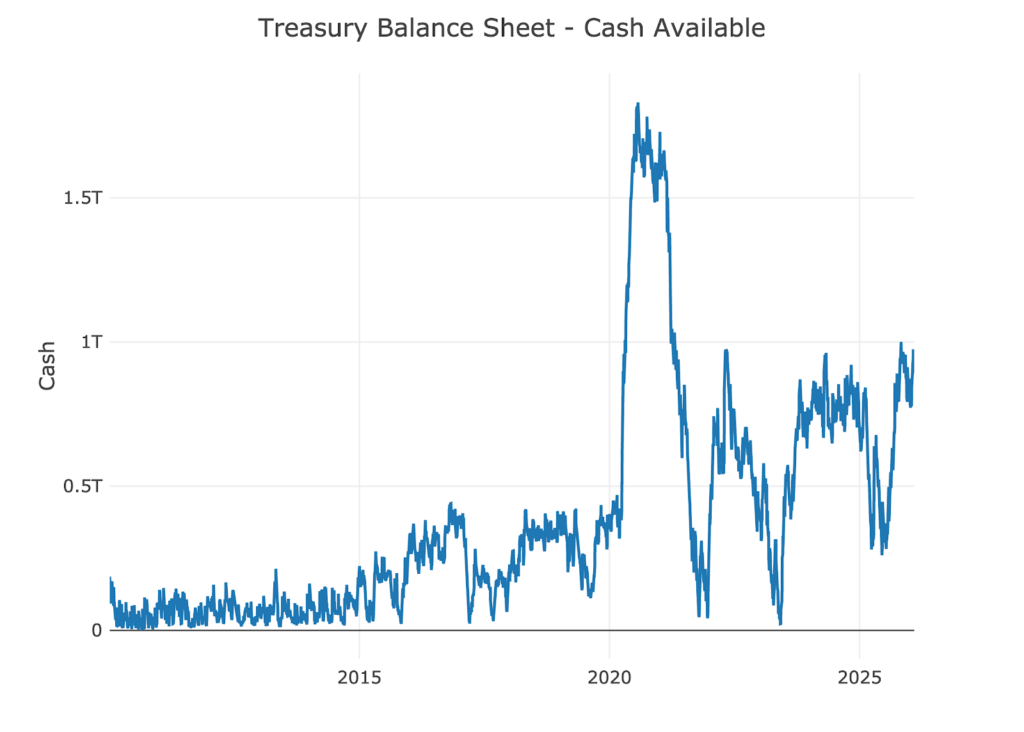

The Treasury has strengthened their cash position to $1T.

Figure: 3 Treasury Cash Balance

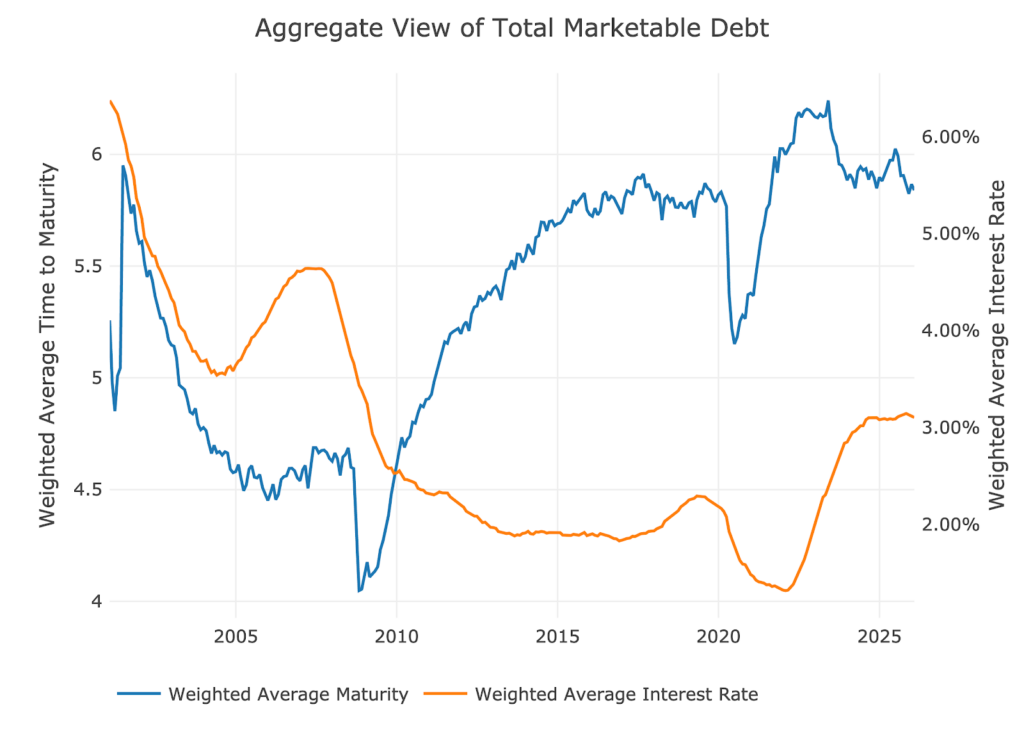

The chart below shows both the maturity of the debt and average interest rate. The blended interest rate has stabilized around 3.1%. More concerning is the average maturity of the debt has dropped to 5.8 years. This is the lowest average rate since 2021. Lower average maturity means the government will have to roll over more debt each year. It increases the risk if the appetite for US debt starts to slow.

Figure: 4 Weighted Averages

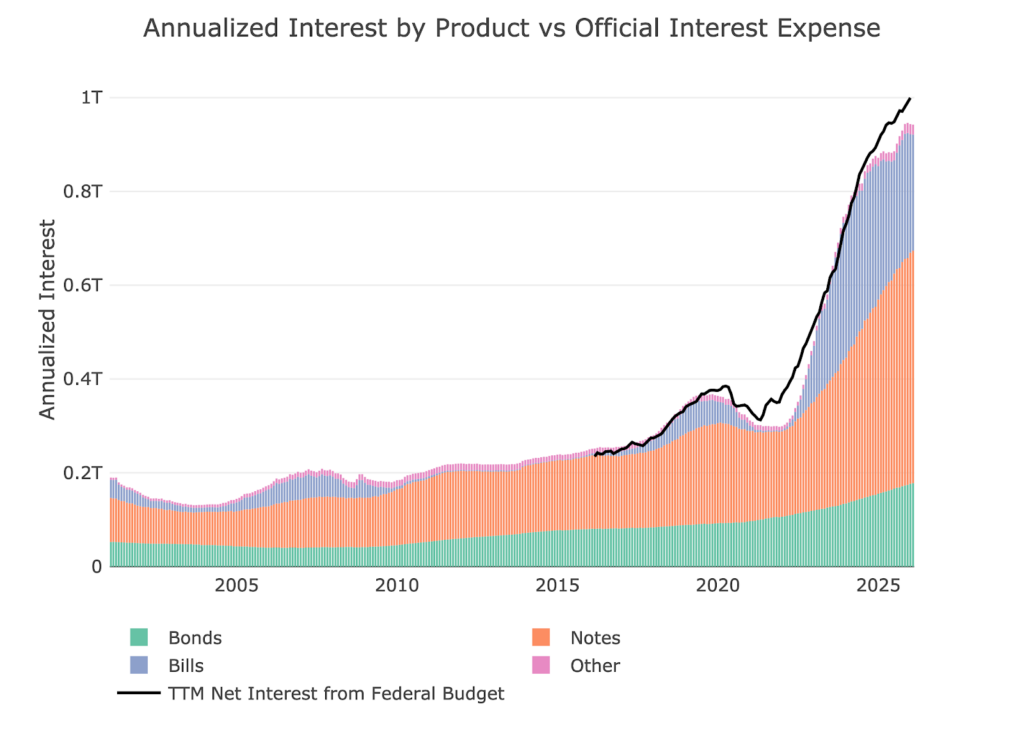

The true danger facing the government is still in the massive interest currently being paid on the debt. It has finally crossed over $1T per year! As shown in the chart, about half of this is concentrated in Notes, which is debt maturing between 2 and 10 years.

Figure: 5 Net Interest Expense

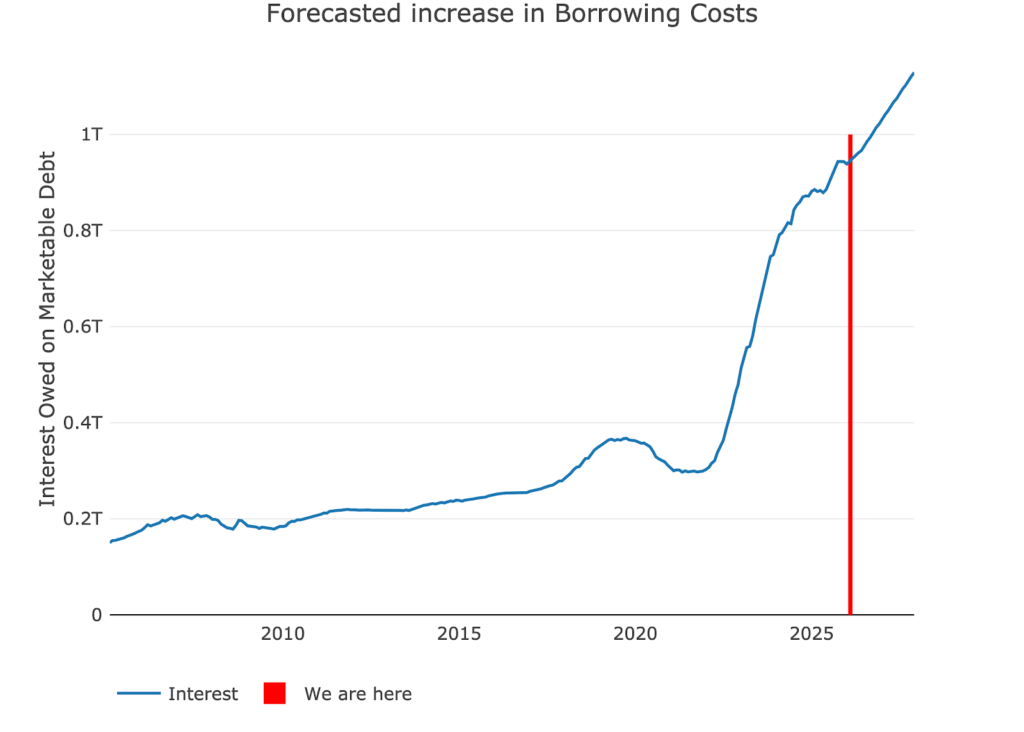

A lot is unknown about how Warsh will manage interest rates, but assuming only one more cut, combined with the rolling maturity of the debt, we can forecast out the cost of the debt going forward. Again, the Treasury left “debt affordability” in the rearview mirror in 2021. The Treasury is now absolutely hemorrhaging cash on debt service costs, set to rise over $1.1T in 2027.

Figure: 6 Projected Net Interest Expense

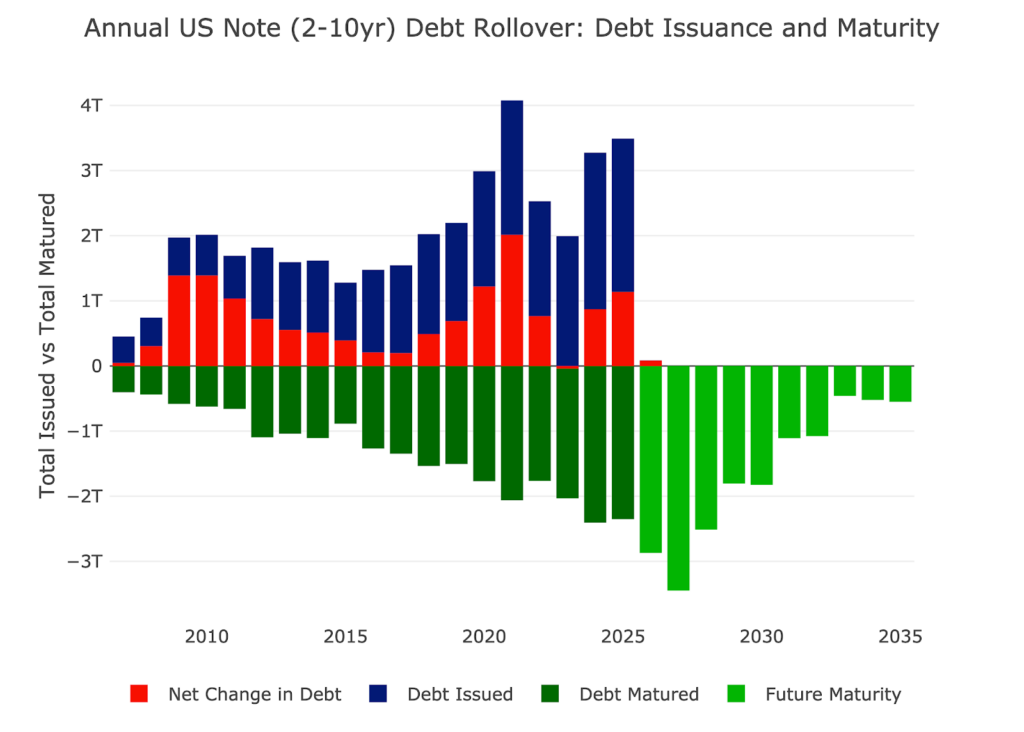

Speaking of debt issuance and rollover, the chart below shows the forecasted debt maturing for 2-10 year maturities. Debt rolling over will be $600B higher in 2026 than it was in 2025. There will be another $500B increase in rollover in 2027.

Note “Net Change in Debt” is the difference between Debt Issued and Debt Matured. This means when positive it is part of Debt Issued and when negative it represents Debt Matured

Figure: 7 Treasury Note Rollover

Yield Curve

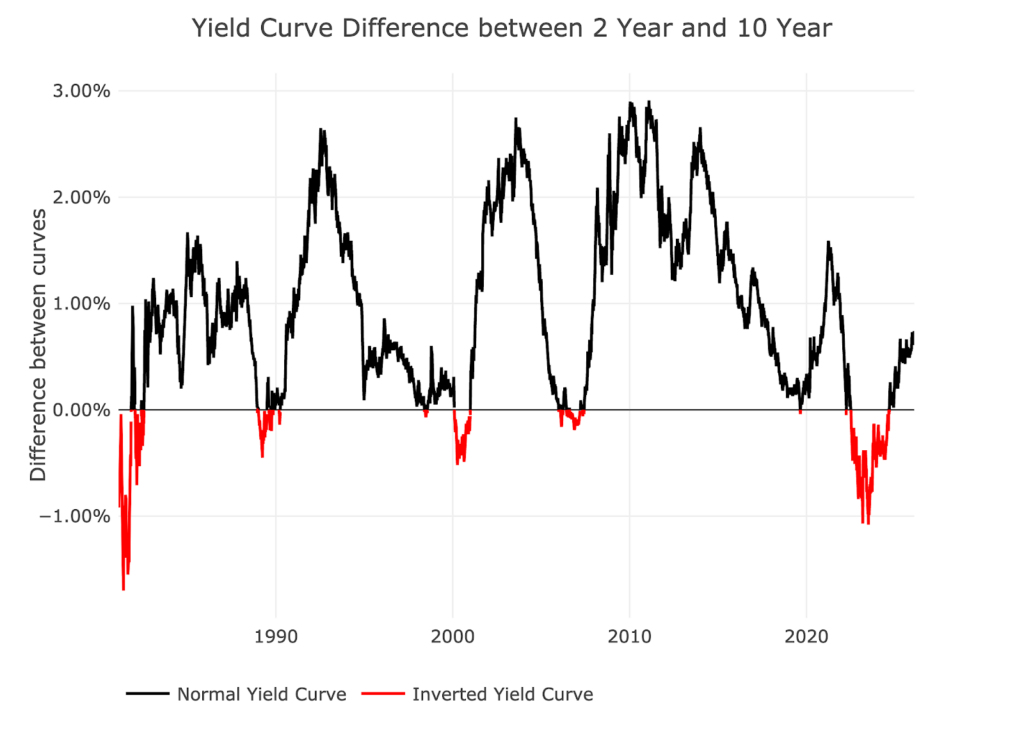

The yield curve has gone back to positive sloping between the 2 and 10 year. The Treasury was borrowing short-term the entire time it was inverted which seems like an odd decision. The current thinking is that Warsh will lower short-term rates and allow more assets to roll off the Fed balance sheet. This will likely steepen the curve which will add more pressure to medium and long-term rates. As shown above, this is where the debt is concentrated which will cause more interest payment pain in future years.

Figure: 8 Tracking Yield Curve Inversion

Historical Perspective

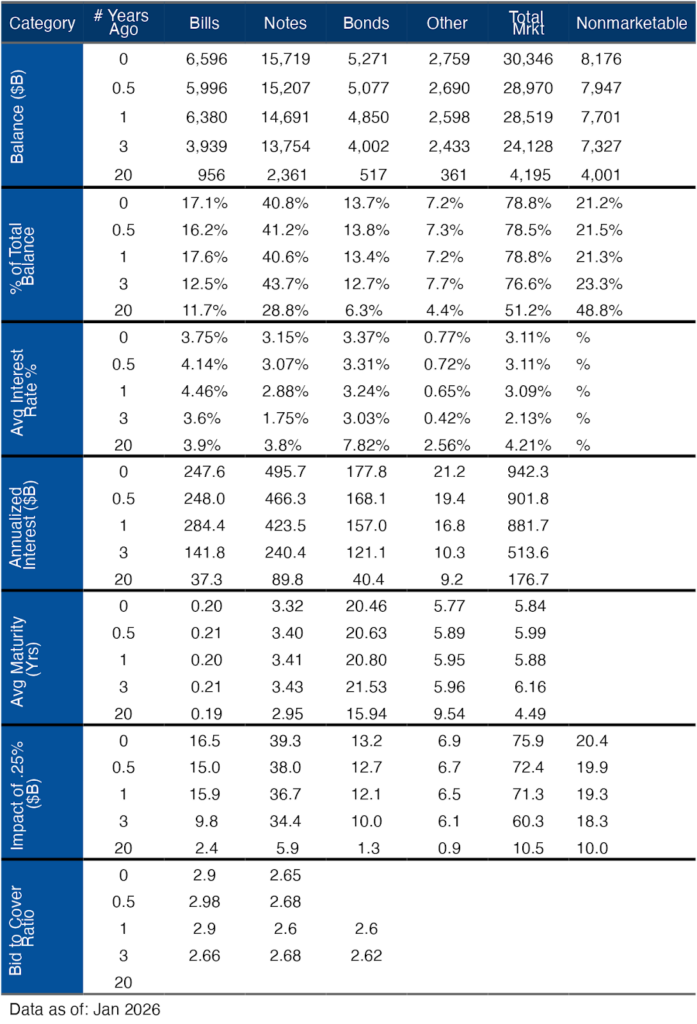

The chart and table below show how the debt and interest has changed over time.

Figure: 9 Total Debt Outstanding

Figure: 10 Debt Details over 20 years

Wrapping Up

Many Fed officials and market pundits have called the current fiscal situation “unsustainable”. This is a gross understatement. The current fiscal situation is an absolute train wreck with no way out. It has been called a ticking time bomb for decades. That bomb has gone off as interest rate expense ballooned higher. It is worse than anyone could have imagined.

The price of gold and silver are screaming this message loud and clear. Warsh may be focused on the short end of the curve, but unless a lid can be put on long-term rates, this train wreck is only going to get worse. At some point, Warsh will walk back his position and being anti-QE. The Fed will be forced to buy on the long end which will only destroy more confidence in the US fiscal situation.