The Fed Balance Sheet Increases by $31B in June

The following analysis breaks down the Fed balance sheet in detail. It shows different parts of the balance sheet and how those amounts have changed. It also shows historical interest rate trends.

Breaking Down the Balance Sheet

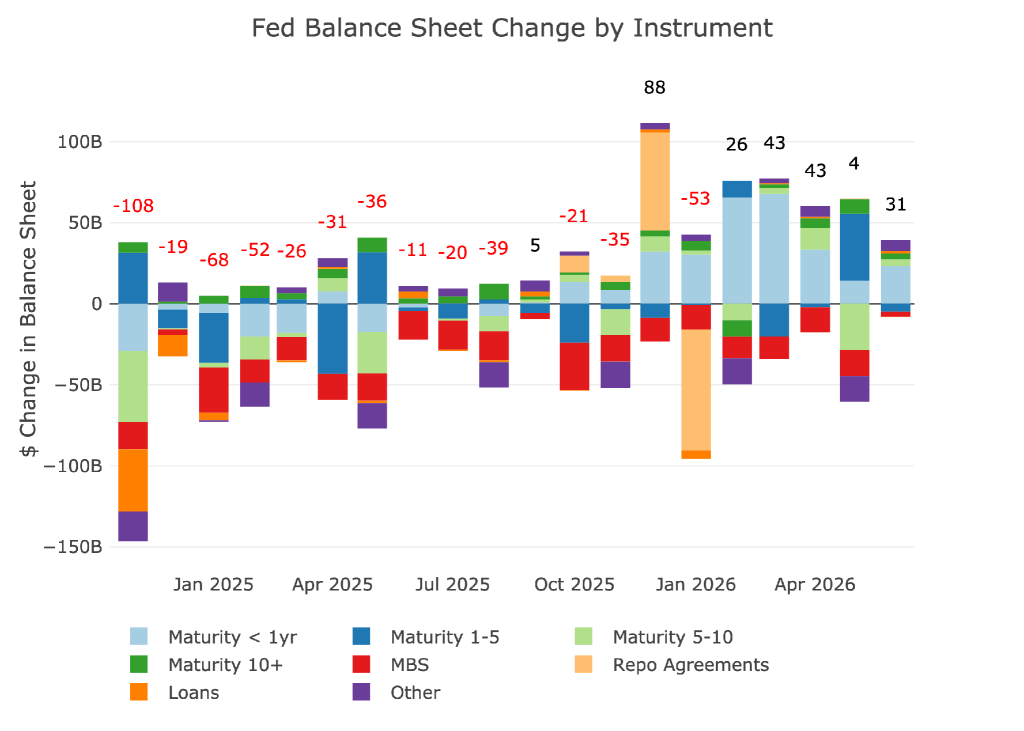

As soon as the Fed ended Quantitative Tightening they launched a new round of Quantitative Easing. As shown in the chart below, the buying has been fairly consistent with 5 consecutive months of increases. The focus has clearly been on the short-end of the curve.

Figure: 1 Monthly Change by Instrument

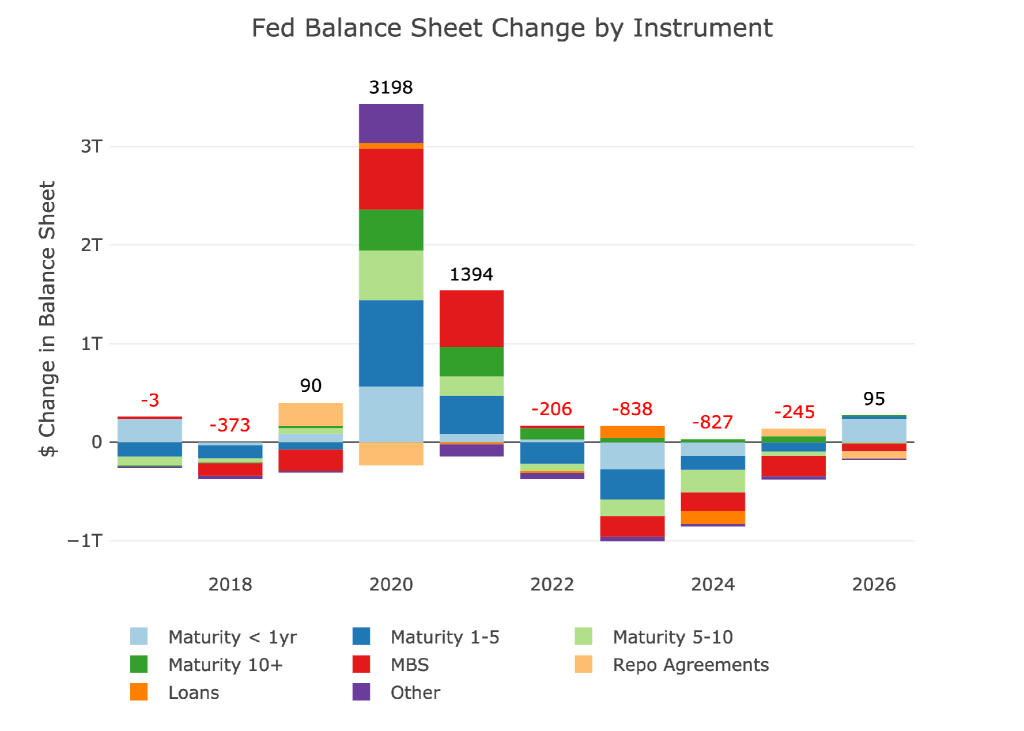

Zooming out to 10 years and grouping the data by year shows the chart below. What you should notice is how quickly the Fed will un-do all the “hard work” in reducing the balance sheet during the next crisis. It took 4 years to reduce the balance sheet about $2.2T. However, in 2020, it took a few months to grow the balance sheet by $3T and 2 years to grow it by $4.5T.

QE has already started despite no clear impending crisis. This is why money supply is growing at the fastest rate since 2021. It’s possible Warsh puts a stop to this usage of the balance sheet, but then the market is going have a harder time moving up as it has been.

Figure: 2 Monthly Change by Instrument

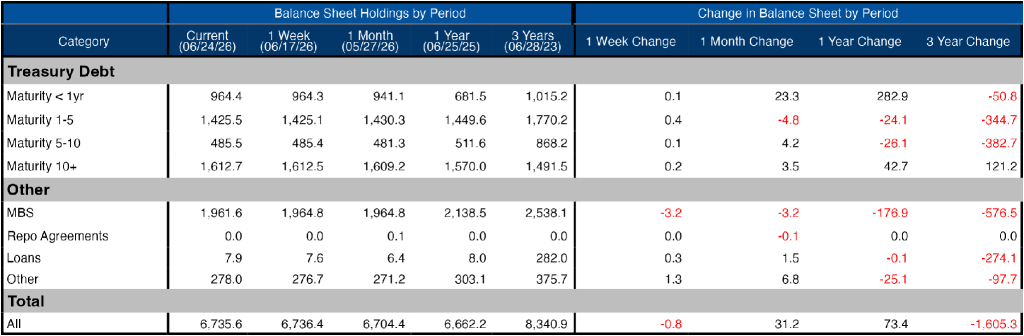

The table below provides more detail on the Fed’s activities and its recent efforts to manage the balance sheet. With QE already resuming, the Fed will be taking a $6.7T balance sheet (and growing) into the next crisis, almost guaranteeing that it will exceed $10T when it fully goes back to QE. Warsh may not like QE, but he will have no choice if he wants to keep the bubble inflated.

Figure: 3 Balance Sheet Breakdown

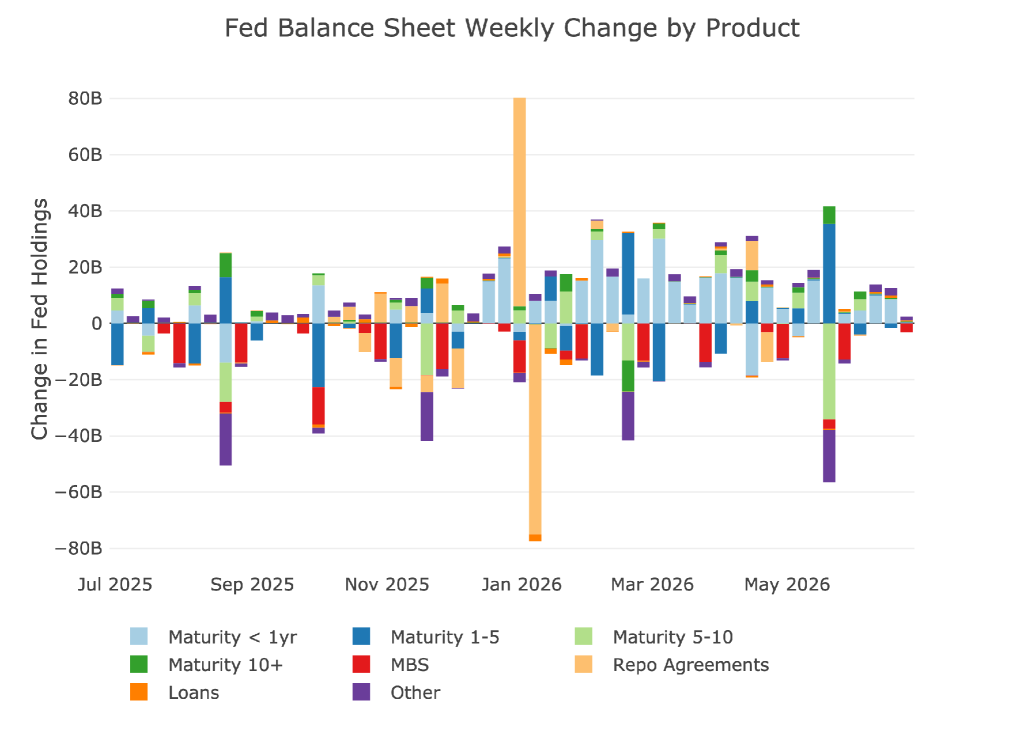

The weekly activity can be seen below. As shown, the Repo agreements were used but then were just as quickly eliminated. According to the Fed, it is not being used as much as they would like to see.

Figure: 4 Fed Balance Sheet Weekly Changes

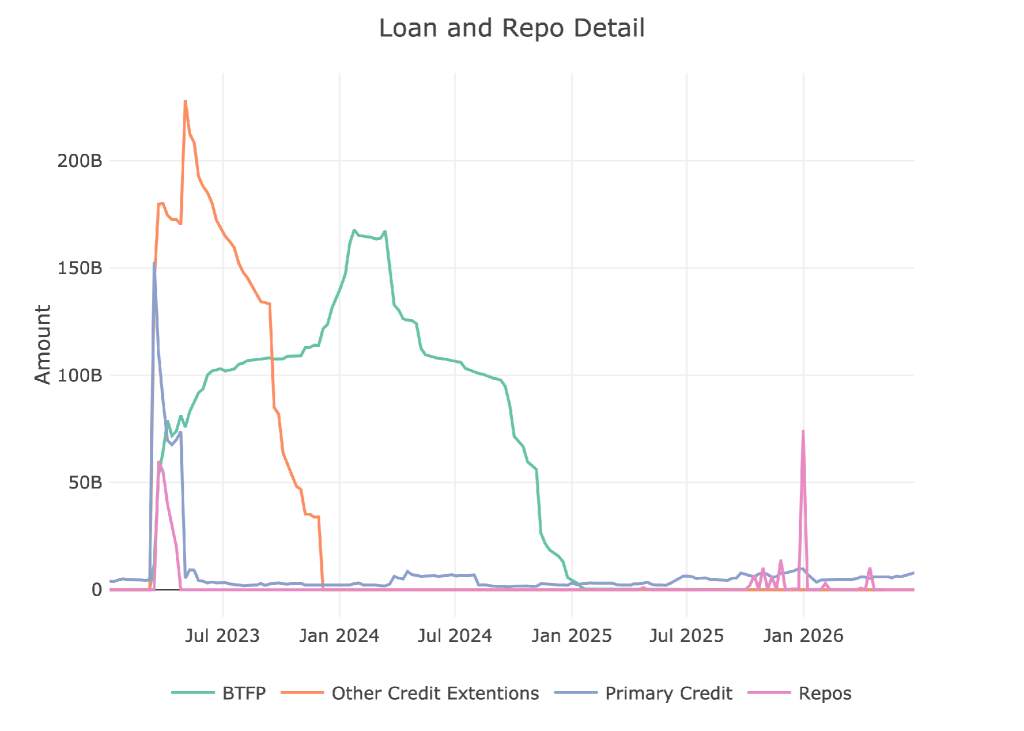

The chart below shows the balance on detailed items in Loans and also Repos. These were the programs set up in the wake of the SVB collapse. All of the programs have dropped down to zero at this point, but as mentioned above, the Fed would like to see more usage of the Repo market (Standard Repo Facility or SRF).

Figure: 5 Loan Details

Yields

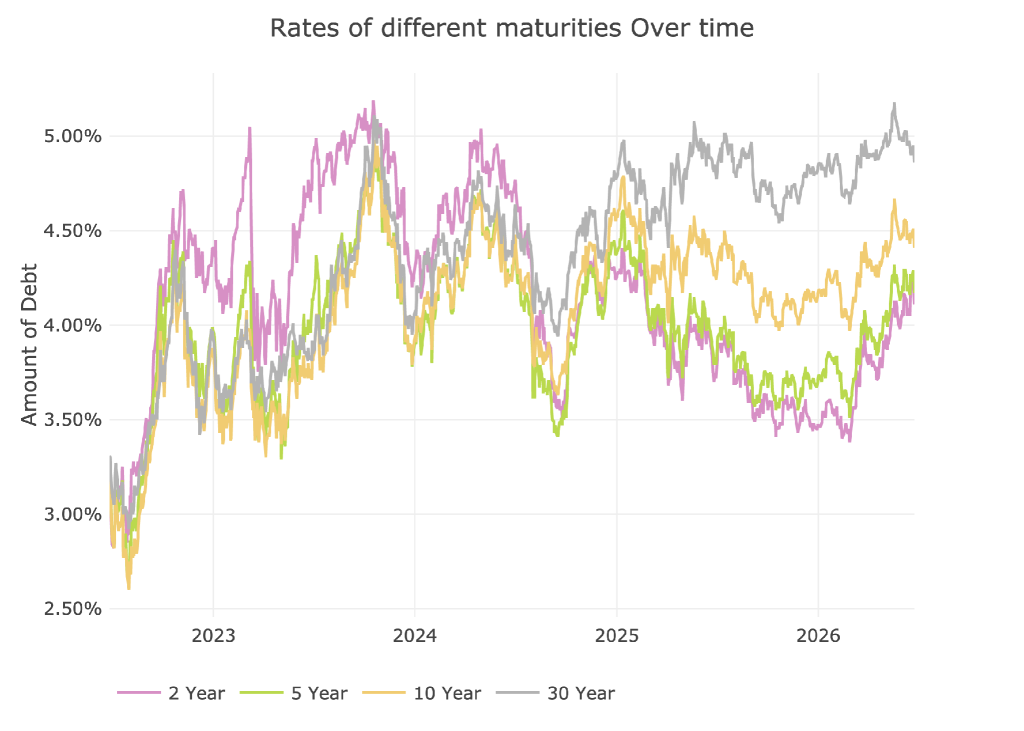

Yields have been fluctuating within a band since Sept 2022, ranging mostly between 3.25% and 4.75%. That range has been broken in the last month with 30-year rates breaking decisively over 5% and the 10-year breaking above 4.5%. The last week has seen rates come down, but it is likely a temporary move. The trend clearly looks to be up.

Figure: 6 Interest Rates Across Maturities

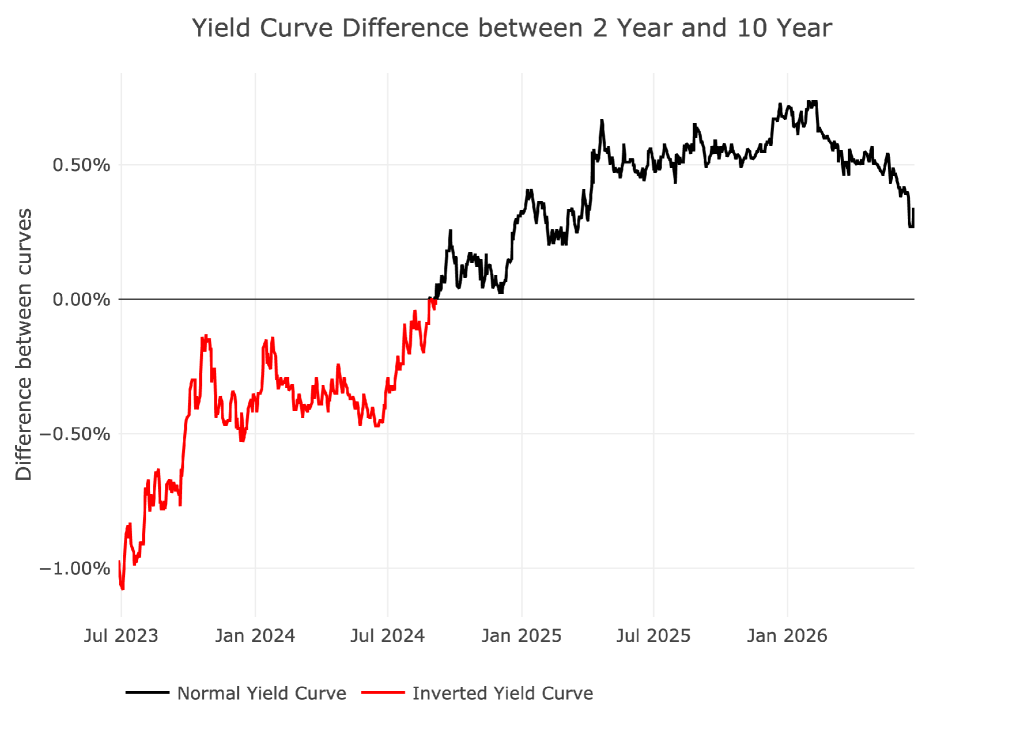

Almost in direct response to the speech Warsh gave, the yield curve started to flatten.

Figure: 7 Tracking Yield Curve Inversion

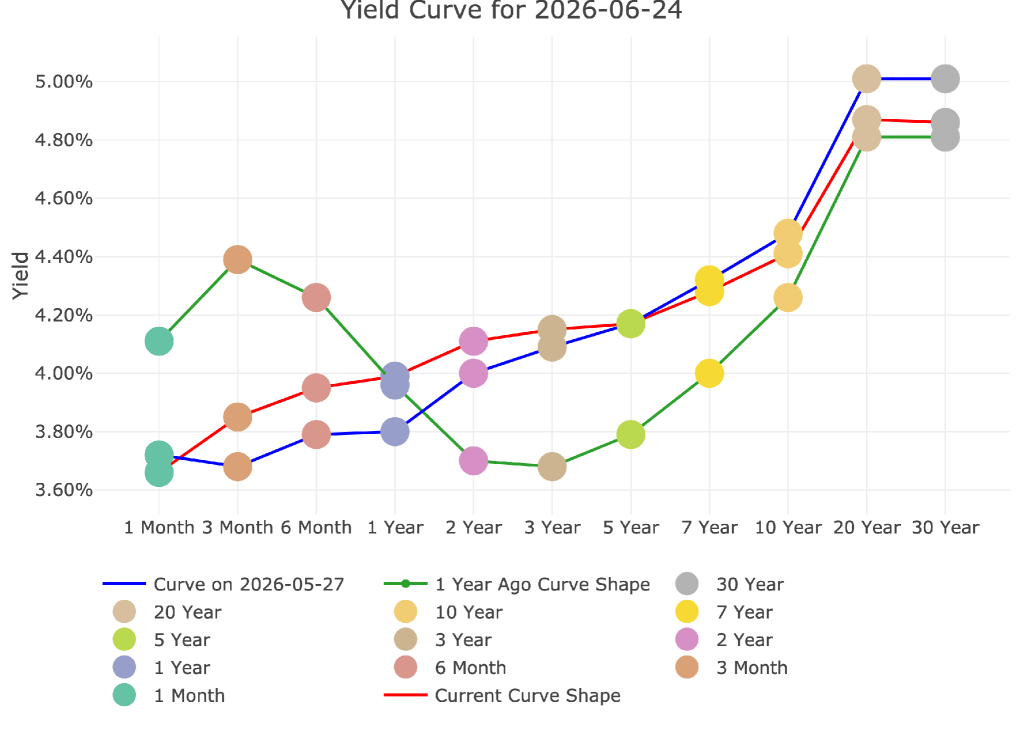

The chart below shows the current yield curve, the yield curve one month ago, and one year ago. When looking at the red line and blue line, it is clear the red line is flattening.

Figure: 8 Tracking Yield Curve Inversion

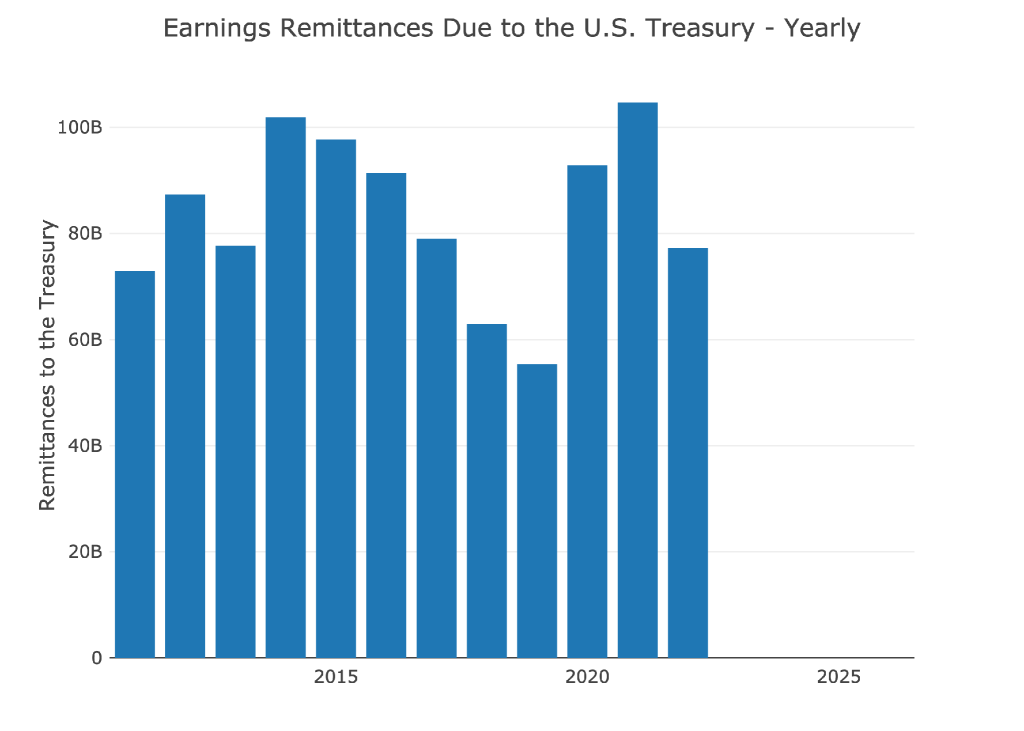

The Fed Takes Losses

When the Fed makes money, it sends it back to the Treasury. This has netted the Treasury close to $100B a year for 10 years. This ended in 2022 when interest rates went up as can be seen below.

Figure: 9 Fed Payments to Treasury

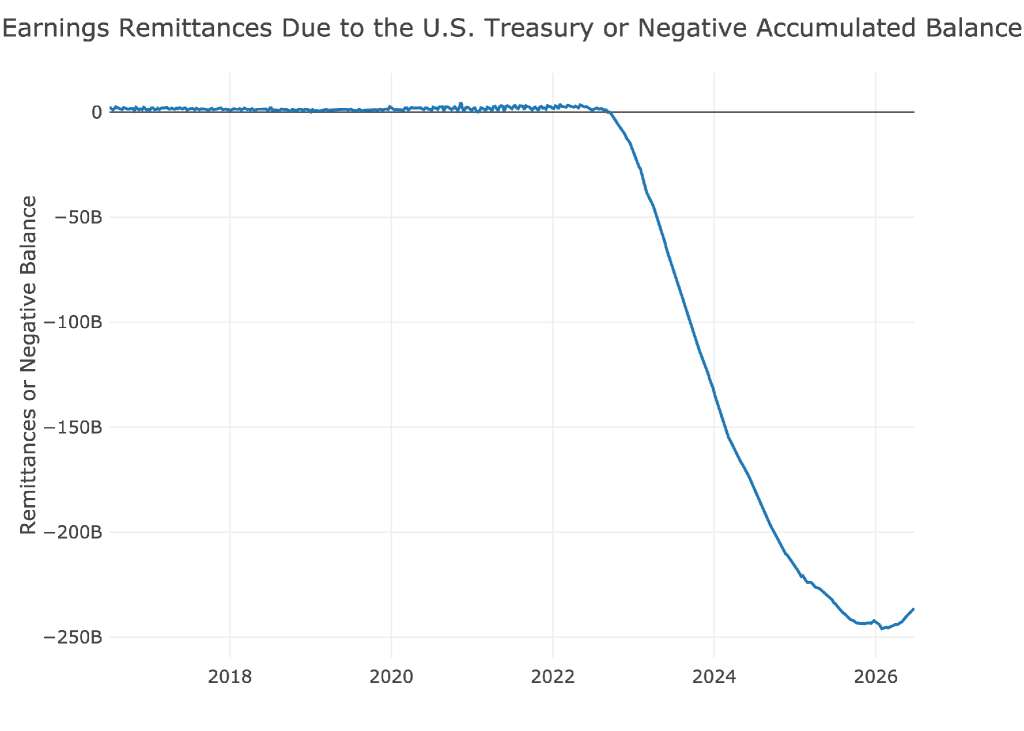

The Fed has been losing money since 2022. As explained: The Federal Reserve Banks remit residual net earnings to the U.S. Treasury after providing for the costs of operations… Positive amounts represent the estimated weekly remittances due to U.S. Treasury. Negative amounts represent the cumulative deferred asset position … deferred asset is the amount of net earnings that the Federal Reserve Banks need to realize before remittances to the U.S. Treasury resume.

Basically, when the Fed makes money, it gives it to the Treasury. When it loses money, it keeps a negative balance by printing the difference. That negative balance exceeded $245B, but has started to turn back up in recent weeks as the Fed has started to make money again. It is still net negative $236B. It will be some time before it pays off the net draw down and is then able to start paying the treasury again.

Figure: 10 Remittances or Negative Balance

Who Will Fill the Gap?

The Fed stopped buying debt in 2022 and have been selling over recent years with QT. However, the Treasury is still issuing tons of new debt. Who has been picking up the slack since the Fed stepped away?

At first, international markets were, but that has changed. Since August of last year, international holders have added a net zero of new Treasury debt. Over that time, the treasury has issued probably close to $2T in debt. Who is going to continue buying up this issuance? Especially when you have so much new equity coming to market through IPOs to crowd out other instruments.

This alone could be the number one reason the Fed has gone back to QE while the treasury has also started issuing more short-term debt.

Note: data is updated on a lag. The latest data is as of April

Figure: 11 International Holders

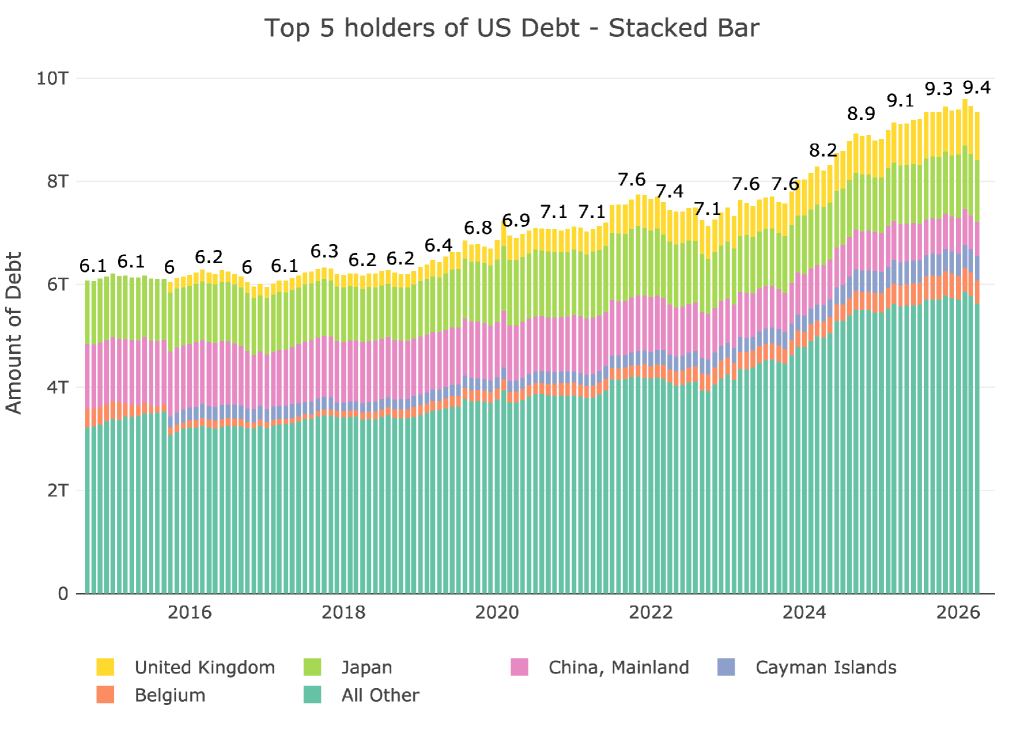

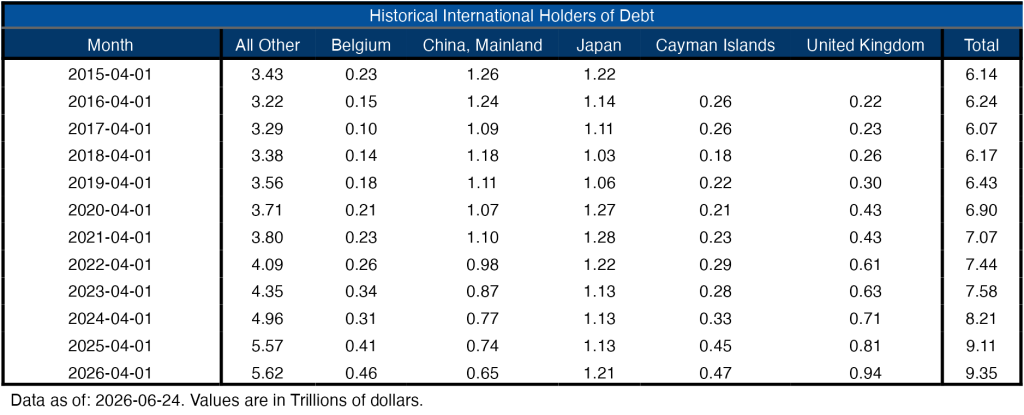

The chart below shows a breakdown of the bigger countries. China’s US Debt holdings have fallen to $650B. The rest of the countries have all added over the last year, but as shown in the chart above, that motion has stopped over the last few months.

Figure: 12 Average Weekly Change in the Balance Sheet

Historical Perspective

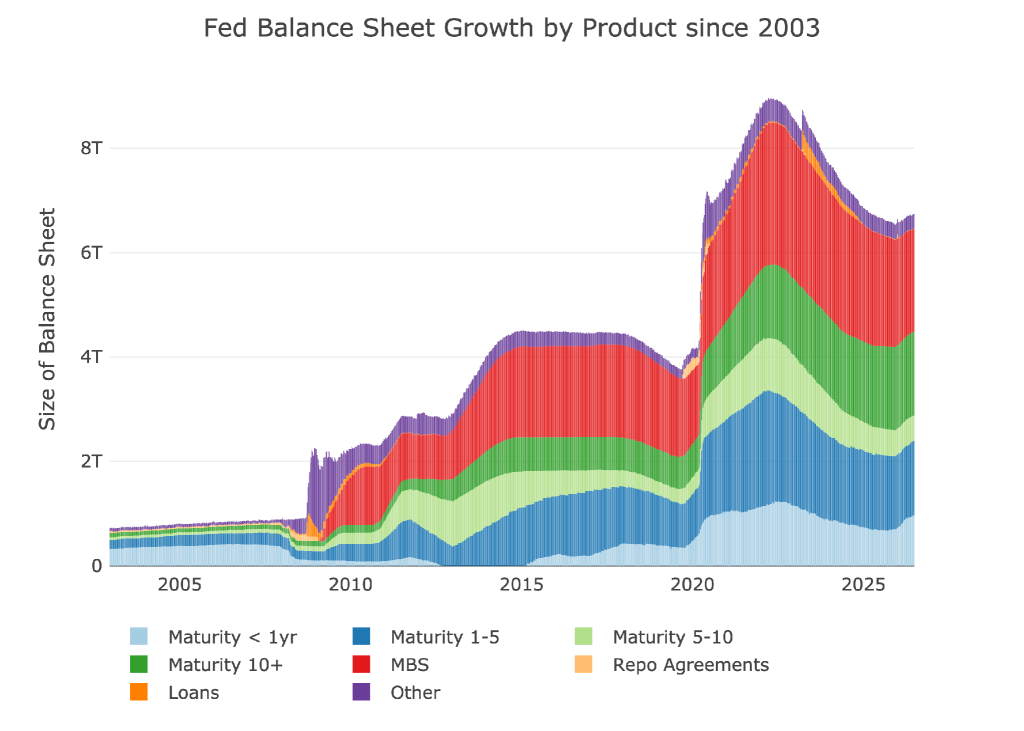

The final plot below takes a larger view of the balance sheet. It is clear to see how the usage of the balance sheet has changed since the Global Financial Crisis. This also highlights the rapid increase and steady decrease. The Fed can never actually shrink its balance sheet back to the previous state, it just does minor reductions when it can before the next crisis blows it up again. Based on the trajectory of the Fed balance sheet, that next crisis might be closer than anyone thinks!

Figure: 13 Historical Fed Balance Sheet

Conclusion

Warsh has come in with a new message: the Fed is ready to get inflation under control. That’s much easier to say than do. When the Treasury issues $2T in debt a year and international buyers are nowhere to be found, someone has to step in. Make no mistake, that will be the Fed. If it isn’t then the consequences will be too great for anyone to bear. When the market figures this out, the precious metals market is going to rebound rapidly.